GST Registration Rejected or Notice Received?

Here’s Exactly How to Fix It in 2026

A step-by-step guide to replying to GST REG-03, REG-17 and ASMT-10 notices, re-filing after rejection, and protecting your registration — updated for CBIC Instruction No. 03/2025-GST.

To reply to

REG-03 notice

Officer decision

after reply

High-risk app

processing limit

Appeal window

under Sec. 107

- Reply deadline is 7 working days from the date of receipt for REG-03 (clarification) and REG-17 (cancellation) notices — missing this triggers automatic rejection via Form GST REG-05.

- CBIC Instruction No. 03/2025-GST (17 April 2025) bars officers from demanding documents beyond the prescribed list in Form REG-01 — any extra demand now requires AC/DC approval. Verify at cbic-gst.gov.in.

- Re-filing after rejection is permitted — submit a fresh Form GST REG-01 via the GST portal at gst.gov.in after correcting the deficiency identified in Form REG-05.

- Appeal under Section 107 must be filed within 3 months of the rejection order — Form APL-01 with a mandatory 10% pre-deposit of the disputed amount.

- Ignoring a GST notice results in ex-parte orders, demand confirmation, possible bank attachment, and registration cancellation.

A GST registration rejected order or an unexpected GST notice can stall your business completely — no GSTIN means no compliant invoicing, no input tax credit, and potential penalties for operating without registration. The good news: most cases of GST registration rejected are fixable, provided you act within the prescribed window and submit the right documents through the correct form on the GST portal.

This guide covers every scenario — from receiving a REG-03 clarification notice during fresh registration, to handling a REG-17 cancellation notice, replying to an ASMT-10 scrutiny notice, and filing an appeal after a final rejection order. All timelines and procedures reflect the latest position as on 06 May 2026, incorporating CBIC Instruction No. 03/2025-GST and Section 74A of the CGST Act.

1 Why GST Registration Gets Rejected: The Most Common Triggers

Understanding why your GST registration was rejected is the first step to an effective fix. Officers scrutinise every Form REG-01 submission and issue a Show Cause Notice in Form GST REG-03 if they find deficiencies. The most frequent rejection triggers in 2025–26 are:

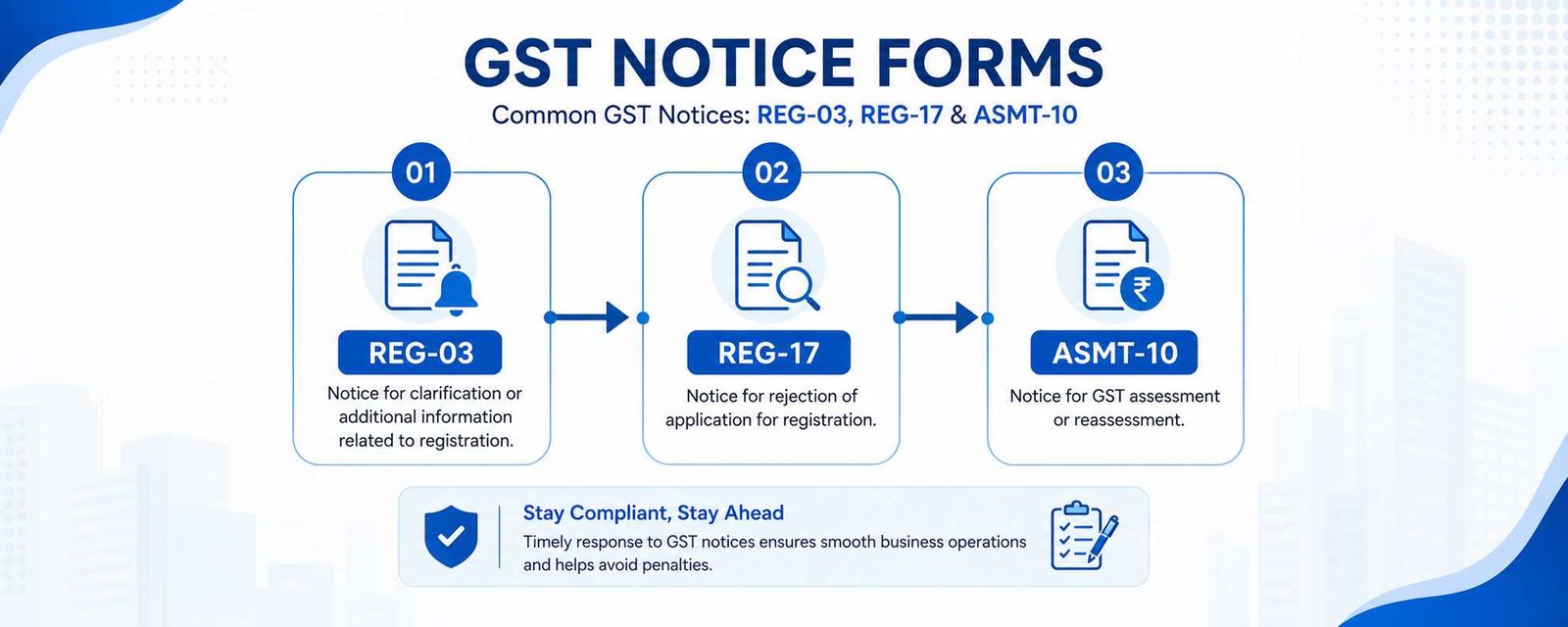

2 GST Notice Types You May Receive: A Quick Reference Table

Not all GST notices are the same. The form number tells you which stage of the process you’re in and which response form to use. Matching the right reply to the right notice is critical — filing the wrong form wastes time and may be treated as non-compliance.

| Notice Form | When Issued | Reply Form | Deadline |

|---|---|---|---|

| GST REG-03 | During fresh registration — officer needs clarification or additional documents | GST REG-04 | 7 working days |

| GST REG-17 | Before suo motu or complaint-based cancellation of existing registration | GST REG-18 | 7 working days |

| GST REG-23 | Before rejection of revocation application (cancellation reversed) | GST REG-24 | 7 working days |

| ASMT-10 | Scrutiny of filed returns — discrepancy between GSTR-1, GSTR-3B, GSTR-2B | ASMT-11 | As specified in notice (typically 30 days) |

| DRC-01 / SCN | Show Cause Notice — proposed tax demand, penalty, or ITC denial | DRC-06 (reply) or DRC-03 (payment) | As specified (typically 30 days) |

| GSTR-3A | Non-filing of returns — demand to file within 15 days | File pending returns immediately | 15 days |

Access all active notices by logging into gst.gov.in → Services → User Services → View Additional Notices and Orders. All notices are displayed in descending order with their reference numbers and due dates.

3 Step-by-Step: How to Reply to a GST REG-03 Notice (Registration Clarification)

Form GST REG-03 is the most common notice new applicants receive. The officer has identified a deficiency — missing documents, address mismatch, or a query about business activity — and you have 7 working days from the date of service to file your reply using Form GST REG-04. Missing this deadline triggers automatic rejection via REG-05.

-

1

Log in to gst.gov.in using your ARN (Application Reference Number) or temporary credentials. Go to Services → User Services → View Additional Notices and Orders.

-

2

Open the REG-03 notice. Read every observation carefully. Download a copy. The notice will specify exactly which documents or clarifications are required — officers are bound by Instruction 03/2025-GST to state specific reasons.

-

3

Prepare your response documents. Match each observation in the REG-03 to the correct document. For a business address query: provide electricity bill, rent agreement with ownership proof of the lessor (if lease is registered, lessor’s ID is not separately required), or property tax receipt.

-

4

File Form GST REG-04 on the portal. Navigate to the REG-03 notice and click Reply. The system will open the REG-04 form. Fill in your clarification in the statement field — be factual, reference the document names you are attaching. Upload all documents in PDF or JPEG format with clear file names.

-

5

Verify with the authorised signatory and file. Select the authorised signatory from the Authorised Signatory tab, check the verification box, and click FILE. Save your acknowledgement number.

-

6

Await the officer’s decision. If your REG-04 reply is satisfactory, registration is approved within 7 working days. If not satisfactory — or if physical verification is ordered — the officer may pass a rejection order in Form GST REG-05 within 7 working days from the date of your reply.

4 GST Registration Rejected via REG-05: What Happens Next

Receiving Form GST REG-05 means the officer has rejected your registration application. The rejection order must, by law, state specific reasons. You have two routes available immediately after a GST registration rejected order is issued.

Correct the deficiency identified in the REG-05 order and file a fresh Form GST REG-01 on gst.gov.in. There is no waiting period or bar on re-application. This is the fastest route when the rejection was due to document issues or a correctable error.

Timeline: Re-application is processed fresh — 7 working days for standard (Aadhaar-authenticated) applications.

If you believe the rejection was legally unsound — vague reasons, unlawful document demands, or violation of natural justice — file an appeal in Form APL-01 to the Appellate Authority. The window is 3 months from the date of the rejection order.

Pre-deposit: Typically 10% of the disputed amount (confirm on portal at filing). The Appellate Authority issues its order in Form APL-04.

In a significant ruling of February 2026, the Gauhati High Court held that a GST cancellation order based on a vague Show Cause Notice — one that merely reproduced statutory provisions without disclosing specific tax periods, invoices, or ITC quantum — is unsustainable in law and violates principles of natural justice. If your REG-05 order lacks specific reasons, this precedent supports a legal challenge.

5 How to Reply to a REG-17 Cancellation Notice

Form GST REG-17 is issued when the tax officer intends to cancel your existing GST registration — either suo motu or following a complaint. The stakes are higher here: cancellation means you cannot issue GST-compliant invoices, lose ITC entitlement going forward, and may face retrospective liability.

You have 7 working days from the date of service to file your reply in Form GST REG-18. The reply must clearly explain why your registration should not be cancelled. If the reply is found satisfactory, the officer drops the proceedings and passes an order in Form GST REG-20. If not, cancellation is confirmed via Form GST REG-19 — issued within 30 days from the date of your reply.

Common grounds for REG-17 notices and how to address them:

| Cancellation Ground | What to Include in REG-18 Reply |

|---|---|

| Non-filing of returns for 6+ months (regular) or 3+ quarters (composition) | File all pending returns before or along with the reply. Attach proof of filing and payment of late fees, interest, and outstanding tax. If returns can’t be filed immediately, explain the reason with a committed timeline. |

| Business not found at registered address | Submit updated address proof — electricity bill (latest), registered rent agreement, and photographs of the business premises. If you’ve relocated, amend your registered address via Form REG-14 before replying. |

| Obtaining registration through fraud / misrepresentation | This is the most serious ground. Provide a factual rebuttal with documentary evidence. Seek professional legal assistance — a poorly drafted REG-18 on this ground can be used against you in adjudication proceedings. |

| Voluntary cancellation request from the registered person | If it’s your own application (Form REG-16), no reply is needed — the REG-17 is procedural. If you did not apply and received REG-17 unexpectedly, raise this discrepancy explicitly in your REG-18 reply. |

6 Replying to an ASMT-10 Scrutiny Notice for Return Discrepancies

An ASMT-10 notice is issued under Section 61 of the CGST Act, 2017 when the officer identifies discrepancies in your filed returns — typically a mismatch between GSTR-1 (outward supplies), GSTR-3B (summary return), and GSTR-2A/2B (auto-populated ITC). Your response must be filed in Form ASMT-11 within the timeframe specified in the notice (usually 30 days).

The ASMT-10 is a pre-demand notice. It is not yet an SCN. Responding accurately and completely to ASMT-10 can prevent escalation to a full Show Cause Notice under Section 73 or the newly restructured Section 74A — the unified provision effective from FY 2024–25 onwards for periods from 01 August 2024.

How to structure an effective ASMT-11 reply:

-

1

Download and analyse the ASMT-10. Identify each specific discrepancy. Cross-reference your GSTR-1, GSTR-3B, and GSTR-2B data for the relevant tax periods. Do not guess — base every statement on reconciled data.

-

2

Prepare a reconciliation statement. Show the values as per GSTR-1, GSTR-3B, and GSTR-2B side by side. Identify whether the discrepancy arises from a timing difference, a genuine error, or a vendor non-filing issue on GSTR-2B.

-

3

Categorise your response. For each discrepancy: (a) accept it and pay the differential tax, interest, and penalty via DRC-03 before filing ASMT-11, or (b) contest it with documentary evidence (invoices, e-way bills, payment proofs, books of accounts).

-

4

File ASMT-11 on the portal. Navigate to Services → User Services → View Additional Notices and Orders, open the ASMT-10, click Reply, and file Form ASMT-11. Attach your reconciliation, supporting invoices, and DRC-03 challan if you’ve made a voluntary payment.

-

5

If the officer is satisfied, no further action is taken. If discrepancies remain unresolved, the officer may issue a Show Cause Notice (DRC-01). Under Section 74A, voluntary payment within 60 days of SCN issuance significantly reduces the penalty.

Facing a GST Notice or Registration Rejection?

Validraft’s GST compliance team drafts REG-04, REG-18, ASMT-11, and appeal replies — accurate, on time, and portal-ready.

Get Expert Help → GST Services7 What CBIC Instruction No. 03/2025-GST Means for Your GST Registration Case

Issued on 17 April 2025 under F. No. CBIC-20016/24/2025-GST, Instruction No. 03/2025-GST replaced the earlier Instruction 03/2023-GST. It is now the operative standard for how every GST REG-01 application must be processed across all field formations. If your application was GST registration rejected or you received a REG-03 notice with demands that appear excessive, this instruction is your primary reference.

8 Consequences of Ignoring a GST Notice: What the Law Provides

Every GST notice carries a legally prescribed response window. Ignoring it is not a neutral act — the CGST Act, 2017 provides specific adverse consequences at each stage, which escalate the longer non-compliance continues.

| Ignored Notice | Consequence | Legal Provision |

|---|---|---|

| REG-03 (no REG-04 reply) | Automatic rejection via REG-05 within 7 working days | Rule 9, CGST Rules 2017 |

| REG-17 (no REG-18 reply) | Registration cancelled ex-parte — REG-19 issued within 30 days | Section 29, CGST Act 2017 |

| ASMT-10 (no ASMT-11 reply) | Escalation to Show Cause Notice — tax demand with interest and penalty | Section 61, CGST Act 2017 |

| DRC-01 / SCN (no reply) | Ex-parte demand order confirmed; penalty up to 100% of tax (fraud); bank account attachment; prosecution under Section 132 | Sections 73, 74A, 79, 132 |

| GSTR-3A (no returns filed) | Best judgement assessment; late fees; registration cancellation after 15 days | Section 46, CGST Act 2017 |

Under Section 74A (operative from 01 August 2024 for FY 2024–25 onwards), the penalty structure was restructured. Voluntary payment before the SCN is issued carries zero penalty. Payment within 60 days of the SCN date reduces the penalty significantly. Every day of delay reduces your options and increases financial exposure.

9 Final Steps: A Checklist Before You File Your GST Notice Reply

Whether your GST registration was rejected or a notice arrived for an existing registration, the response strategy is the same: act within the prescribed window, address each observation specifically with documentary support, and file through the correct form on gst.gov.in. A comprehensive, well-documented GST notice reply prevents escalation in the vast majority of cases.

- Identify the notice form — REG-03, REG-17, ASMT-10, or DRC-01 — and confirm the correct reply form and filing path on the portal.

- Count the working days. The clock starts from the date of service, not the date you noticed it. File before the 7-working-day or 30-day deadline.

- Address every observation. Do not ignore any query in the notice. Unanswered observations are treated as conceded by the officer.

- Attach correctly named documents. Use descriptive file names (e.g., “ElectricityBill_April2026.pdf”) — the officer reviews multiple submissions and clear naming reduces back-and-forth.

- If voluntary payment is appropriate, pay via DRC-03 before or alongside filing your reply — it converts penalty liability from 100% to nil or reduced under Section 74A.

- Cite CBIC Instruction 03/2025-GST in your REG-04 reply if the REG-03 demands documents outside the permitted list — this is a factual and legally accurate ground for objection.

- Save all acknowledgements — ARN, filing confirmation, and the auto-generated reply receipts. These are essential if you later need to file an appeal under Section 107.

Fixing a GST registration rejected outcome is fully achievable through the portal — no visits to GST offices are required for standard cases. The combination of CBIC Instruction No. 03/2025-GST and the digitalised GST notice reply process has made resolution faster when the right steps are followed. Where the officer’s action is legally untenable — vague SCNs, excess document demands, or mechanical orders — the appellate pathway under Section 107 and judicial review remain available.

For businesses that cannot afford prolonged GSTIN disruption, timely expert assistance on GST notice reply drafting and portal filing is the most practical safeguard — far less costly than the penalties and business disruption that accumulate when notices are left unanswered.

Don’t Let a GST Notice or Rejection Stall Your Business

Validraft’s GST team handles REG-03, REG-04, REG-18, ASMT-11, and Section 107 appeals — filed accurately and on time.

Talk to a GST Expert → View GST Services10 Frequently Asked Questions: GST Registration Rejected & GST Notice Reply

Yes. There is no statutory bar on re-applying after a GST registration rejected order. You can file a fresh Form GST REG-01 on gst.gov.in immediately after correcting the deficiency identified in the REG-05 order. The new application is treated as a fresh submission — it is processed within 7 working days if Aadhaar authentication is completed successfully and documents are in order.

Missing the 7 working day deadline for filing Form GST REG-04 results in automatic rejection of your registration application via Form GST REG-05. At that point, your options are: (a) file a fresh REG-01 application after correcting the identified issue, or (b) file an appeal in Form APL-01 under Section 107 of the CGST Act within 3 months of the rejection order date, if you believe the original REG-03 notice was unlawful. The appeal requires a mandatory pre-deposit. The GST notice reply must be filed through the portal — physical submissions are not accepted.

No. Under Rule 9 of the CGST Rules 2017, Form GST REG-05 (rejection order) must state the grounds for rejection. CBIC Instruction No. 03/2025-GST (issued 17 April 2025) reinforces that rejections must be specific and documented. A February 2026 Gauhati High Court ruling (WP(C) No. 878/2026) held that a GST cancellation order that merely reproduces statutory provisions without specifying the tax period, invoices, or ITC quantum violates principles of natural justice and is legally unsustainable. If your GST registration rejected order lacks specific reasons, you have a strong legal basis for appeal.

Log into gst.gov.in → Services → User Services → View Additional Notices and Orders. Open the ASMT-10 and download it. Prepare a reconciliation of the discrepancies identified — compare your GSTR-1, GSTR-3B, and GSTR-2B data. File your GST notice reply in Form ASMT-11 within the deadline stated in the notice (typically 30 days). If some discrepancies are valid, pay the differential tax, interest, and applicable penalty via Form DRC-03 before or alongside filing ASMT-11. Under the restructured Section 74A, voluntary payment within 60 days of any subsequent SCN substantially reduces the penalty.

Ignoring a DRC-01 Show Cause Notice results in an ex-parte demand order — the tax liability is confirmed along with interest and penalty. Under Section 74A of the CGST Act 2017 (operative from 01 August 2024), the penalty can range from 10% to 100% of the tax demand depending on intent and timing of voluntary compliance. Continued non-compliance can trigger bank account attachment under Section 79, provisional attachment of assets, and in cases of deliberate fraud, criminal prosecution under Section 132. Filing a timely and accurate GST notice reply is always preferable to allowing an ex-parte order.

Yes — GST registration can be cancelled suo motu by the officer on grounds including non-filing of returns for 6 consecutive months (regular taxpayer) or 3 consecutive quarters (composition taxpayer), business not found at registered address, or registration obtained through fraud or misrepresentation. Even if the ground is disputed, the REG-17 notice must be replied to within 7 working days in Form REG-18. If cancellation has already been ordered, apply for revocation in Form REG-21 within 30 days — but only after filing all pending returns and clearing all dues including tax, interest, and late fees. Verify the revocation process at gst.gov.in.

📎 Authoritative Sources

- → GST Portal — Form REG-01, REG-03, REG-04, REG-05, REG-17, REG-18, ASMT-10, ASMT-11

- → CBIC — Central Board of Indirect Taxes and Customs (Official)

- → CBIC Instruction No. 03/2025-GST — F. No. CBIC-20016/24/2025-GST, dated 17 April 2025 (PIB)

- → GST Portal User Guide — Filing Clarification (REG-04)

- → GST Portal User Guide — View Notices and Demand Orders