Director Disqualification in India:

Causes, Consequences & How to Restore Status in 2026

Your DIN is deactivated. Every directorship you hold is at risk. Here is the complete 2026 guide to understanding director disqualification India rules, what happens next, and the exact steps to restore director status — including the CCFS 2026 amnesty window open until 15 July 2026.

Disqualification

Period

Consecutive Non-Filing

Triggers Section 164(2)

Fee Waiver Under

CCFS 2026

CCFS 2026

Deadline

- Three consecutive years of non-filing under Section 164(2) of the Companies Act 2013 triggers automatic director disqualification India — affecting every directorship you hold, not just the defaulting company.

- DIN gets deactivated by MCA the moment disqualification is triggered — you cannot file any MCA form, sign resolutions digitally, or be named in any ROC document until restored.

- CCFS 2026 (General Circular 01/2026, dated 24 February 2026) offers a 90% waiver on accumulated additional fees. Window: 15 April to 15 July 2026. Use it to file pending AOC-4 and MGT-7 before disqualification is formally triggered. Verify at mca.gov.in.

- To restore director status after disqualification: file all pending returns, apply for DIN reactivation via DIR-10, and — if the company is already struck off — file for NCLT restoration under Section 252 within 3 years of strike-off date.

- Disqualification is public record — MCA publishes the list of disqualified directors by jurisdiction at mca.gov.in/disqualified-directors. Investors, lenders, and partners can check your DIN status instantly.

Director disqualification India is not a distant compliance risk — it is an active enforcement mechanism that MCA has been applying with increasing precision since 2017. If your company has not filed its annual returns for three consecutive years, your DIN is already at risk of being deactivated, regardless of whether the company is operational. Understanding director disqualification India under Section 164 of the Companies Act 2013 is now essential for every director, promoter, and compliance officer.

This guide covers all grounds of disqualification under Section 164(1) and 164(2), the exact consequences once DIN is deactivated, and the complete step-by-step process to restore director status in 2026 — including the limited-time CCFS 2026 window, the DIR-10 reactivation process, and NCLT restoration for struck-off companies.

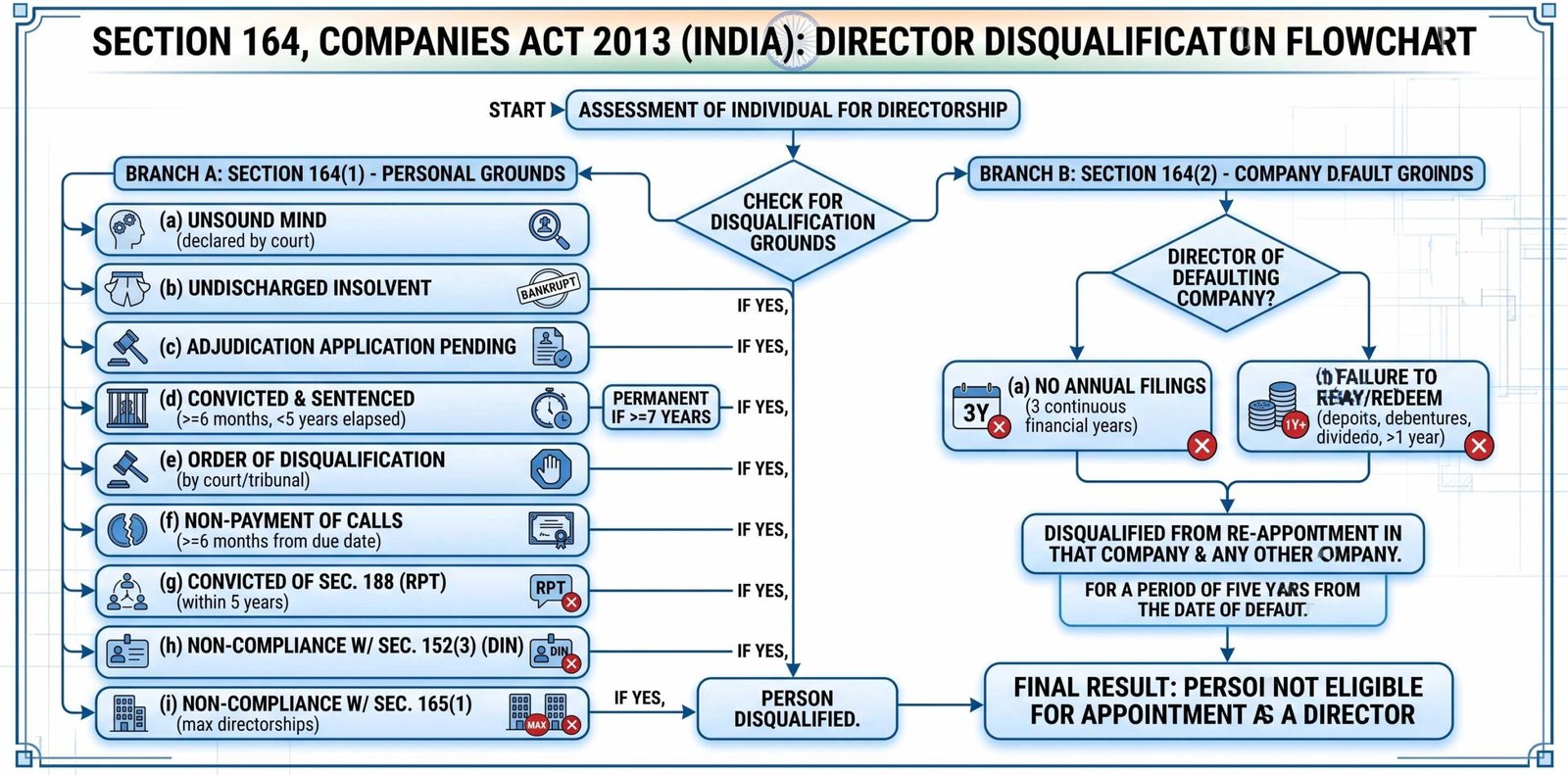

1 What Is Director Disqualification Under Section 164?

Section 164 of the Companies Act 2013 governs director disqualification India. It operates on two distinct tracks — personal disqualification under Section 164(1) and company-default-triggered disqualification under Section 164(2). Both result in DIN deactivated status and bar the individual from holding any directorship in India for the applicable disqualification period.

Section 164(1) — Personal Grounds

A person is ineligible for appointment as director if they meet any of the following conditions:

Section 164(2) — Company-Default Grounds

This is the most commonly triggered ground of director disqualification India. A director becomes disqualified for 5 years if the company in which they are a director has:

- Not filed financial statements (AOC-4) or annual returns (MGT-7) for three consecutive financial years. This is the primary trigger behind mass DIN deactivations since 2017.

- Failed to repay deposits accepted or the interest due thereon for a continuous period of one year or more.

- Failed to redeem debentures on the due date or pay interest due thereon for a continuous period of one year or more.

- Failed to pay a declared dividend for more than one year.

2 Consequences of Director Disqualification India — What Happens When DIN Is Deactivated

When MCA triggers director disqualification India and marks your DIN as deactivated, the consequences are immediate, multi-layered, and public. Here is every impact a disqualified director faces:

⛔ Vacate All Directorships

- You must vacate your position in every company where you hold a directorship — not just the defaulting entity.

- This includes Pvt Ltd, Public Ltd, Section 8, OPC, and any other registered companies.

- The company must formally update ROC records to reflect the vacancy.

🔐 DIN Deactivated — Full Digital Lockout

- A deactivated DIN prevents you from filing any e-form on the MCA portal.

- You cannot sign board resolutions digitally or be named in any compliance submission.

- Your digital identity as a director ceases to function until DIN is restored.

🚷 No New Appointments

- You cannot be appointed or re-appointed as director in any company during the 5-year disqualification period.

- Any appointment attempted during this window is void and exposes the company to penalties.

📢 Public Record on MCA Portal

- MCA publishes the list of disqualified directors on mca.gov.in, searchable by DIN.

- Any investor, lender, or partner conducting due diligence can instantly verify your disqualification status.

- Reputational damage is often harder to recover from than the legal status itself.

3 How to Check If Your DIN Is Deactivated — Director Disqualification Status Lookup

Checking your director disqualification India status takes under 2 minutes on the MCA portal. Here is the exact process:

| Step | Action | Where |

|---|---|---|

| 1 | Visit the MCA portal | mca.gov.in |

| 2 | Go to MCA Services → DIN Services | Top navigation menu |

| 3 | Select "Verify DIN / Director Details" | Under Director Services section |

| 4 | Enter your 8-digit DIN number | Search field on the verification page |

| 5 | Check status field — look for "Deactivated" or "Disqualified" | Results screen |

| 6 | Cross-check against the published disqualified directors list | MCA Disqualified Directors List |

The disqualified directors list published by MCA includes the director's DIN, full name, CIN of the defaulting company, and the period of disqualification. If your name appears, the clock on your 5-year bar has already started.

4 CCFS 2026 — The Amnesty Scheme That Can Prevent Director Disqualification India

The Companies Compliance Facilitation Scheme 2026 (CCFS 2026), issued via MCA General Circular 01/2026 dated 24 February 2026, is the single most important intervention available to directors at risk of disqualification in 2026. It is an amnesty window that allows companies to regularise all pending annual filings at 10% of the accumulated additional fee.

| Scenario | Normal Additional Fee | Under CCFS 2026 (10%) | Savings |

|---|---|---|---|

| 1 form, 1 year late | ~₹36,500 | ~₹3,650 | ₹32,850 |

| 2 forms, 2 years late | ~₹1,46,000 | ~₹14,600 | ₹1,31,400 |

| 2 forms, 3 years late | ~₹2,19,000+ | ~₹21,900 | ₹1,97,100+ |

If your company has missed AOC-4 and MGT-7 for two years, the third year of non-filing will trigger Section 164(2) disqualification. CCFS 2026 is the mechanism to file all overdue returns before that threshold is crossed — at a fraction of normal cost.

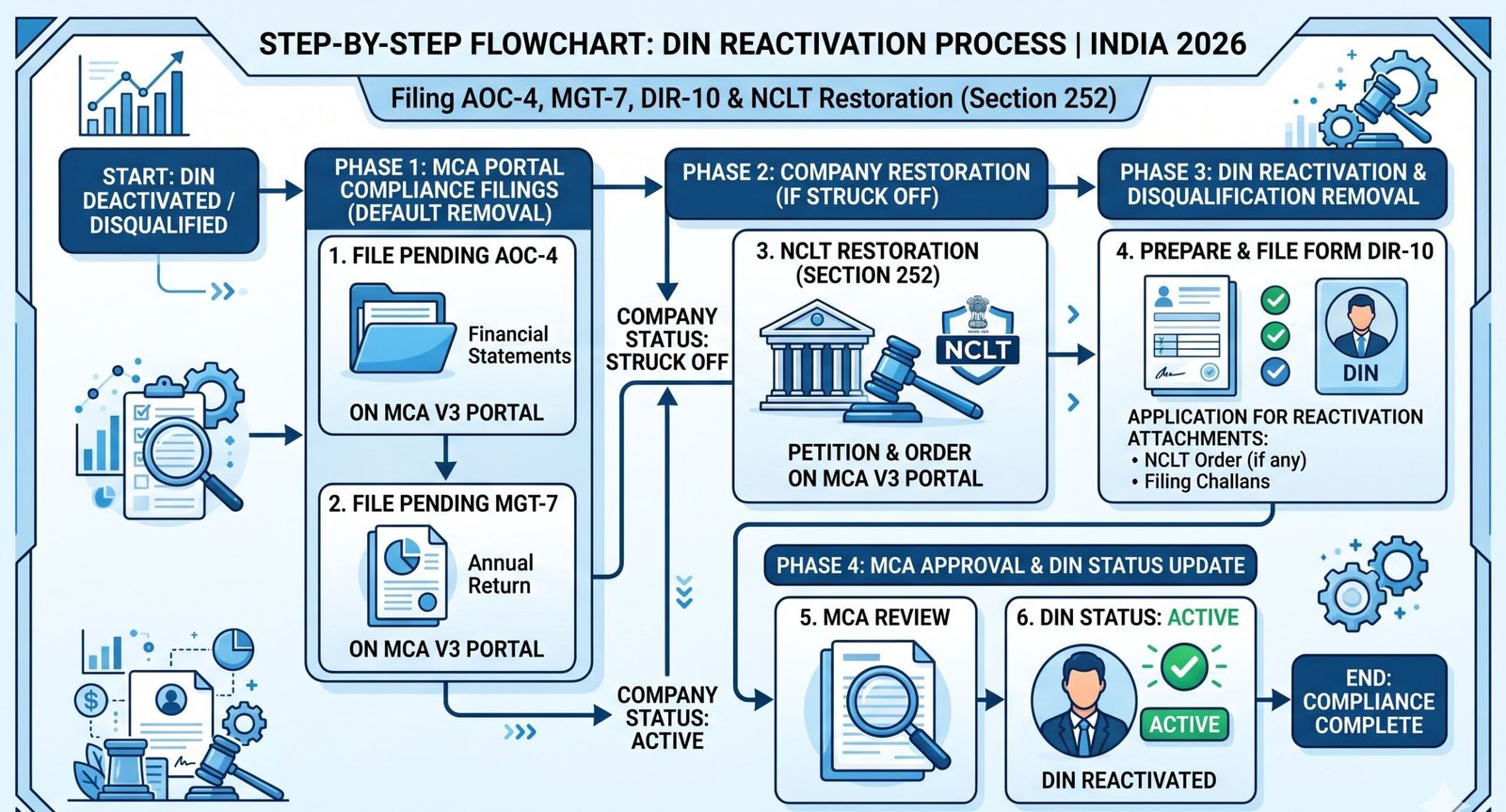

5 How to Restore Director Status in India — Step-by-Step Process 2026

The path to restore director status depends on whether the company is still active or has been struck off. Here is the complete process for both scenarios.

Path A — Company Is Still Active (Not Struck Off)

Path B — Company Has Been Struck Off (Section 248)

If the company was struck off by ROC under Section 248 — typically for two or more years of non-filing — the only legal path to restore director status and revive the company is through NCLT under Section 252 of the Companies Act 2013.

| Aspect | Detail |

|---|---|

| Applicable provision | Section 252, Companies Act 2013 |

| Who can file | Any aggrieved member, creditor, director, or workman of the struck-off company |

| Time limit | Within 3 years from the date of strike-off (gazette notification date) |

| Forum | National Company Law Tribunal (NCLT) bench with jurisdiction over the company's registered office |

| Process | File restoration petition → NCLT hearing → Order for restoration → ROC updates records → Company revived on register |

| Post-restoration | File all overdue returns within the time allowed by NCLT order → Apply for DIN reactivation via DIR-10 |

| Beyond 3 years | No statutory remedy. High Court writ petition is the only remaining option and success is not guaranteed |

6 Can You Appeal Director Disqualification India? — Legal Remedies

The Companies Act 2013 does not provide a direct statutory remedy for removing disqualification under Section 164(2). However, directors have three available legal routes to challenge or mitigate disqualification:

7 Director Disqualification India — Common Causes & How to Prevent Them

Most instances of director disqualification India are entirely preventable. The triggers are well-defined and tied to specific, recurring compliance deadlines. Here is a breakdown of the most common causes and the prevention measure for each:

| Cause | Trigger | Prevention |

|---|---|---|

| Non-filing of AOC-4 + MGT-7 | 3 consecutive financial years | File within 30 days (AOC-4) and 60 days (MGT-7) of AGM each year |

| Inactive company never closed | Non-filing even for a company that never started operations | Strike off or apply for dormant status via MSC-1 immediately |

| DIR-3 KYC not filed | Annual non-filing deactivates DIN (different from Section 164 disqualification) | File DIR-3 KYC by 30 September every year without exception |

| Deposit/debenture default | Failure to repay/redeem for more than 1 continuous year | Maintain repayment schedules; raise internal alerts 60 days before due dates |

| Dividend not paid | Declared dividend unpaid for more than 1 year | Transfer dividend amount to separate account within 5 days of declaration; pay within 30 days |

| Multiple board seats, one default | Default in one company disqualifies you across all companies | Audit filing status of every company where you hold a directorship annually |

8 Director Disqualification India — Special Situations in 2026

Two developments in early 2026 are directly relevant to every director assessing their disqualification exposure:

📋 Corporate Laws (Amendment) Bill 2026

Introduced on 23 March 2026 and currently before the Joint Parliamentary Committee. Proposes a reduced fee structure for delayed ROC filings — potentially replacing the ₹100/day flat rate with a tiered structure. Also proposes further decriminalisation of filing offences. This Bill is not yet enacted. Until it becomes law, the existing ₹100/day additional fee and Section 164 disqualification rules remain fully in effect.

🏢 CCFS 2026 + Section 164(2) Interaction

CCFS 2026 does not cure an existing disqualification — it prevents a new one from being triggered. If your company has missed filings for 2 years, filing under CCFS 2026 before 15 July 2026 stops year 3 from being counted. If disqualification has already been triggered, you still need DIR-10 or NCLT restoration. The CCFS scheme reduces the financial cost of filing but does not automatically restore a deactivated DIN.

DIN Deactivated or Disqualification Notice Received?

Validraft's compliance team handles Section 164 cases, CCFS 2026 filings, DIR-10 reactivation, and NCLT restoration petitions. Act before 15 July 2026 to access the 90% fee waiver window.

Get a Free Consultation → View ROC Compliance Services9 Director Disqualification India — Frequently Asked Questions

10 Conclusion — Act Before 15 July 2026

Director disqualification India under Section 164 is one of the most consequential provisions in corporate law — and one of the most preventable. The MCA's enforcement posture has been consistently strict since 2017, and the publication of disqualified directors on the public portal means there is no quiet path around it. If your DIN has been deactivated or you are approaching three consecutive years of non-filing, the options available to you today are materially better than they will be after 15 July 2026.

CCFS 2026 is an exceptional opportunity to clear a compliance backlog at 90% savings and secure conditional immunity from adjudication proceedings. Whether you need to prevent director disqualification India from being triggered, or you need to restore director status after your DIN was deactivated, the path forward requires the same first step: file all overdue AOC-4 and MGT-7 returns on mca.gov.in before the July deadline. Then follow through with DIR-10 reactivation and, where necessary, NCLT restoration under Section 252.

The compliance calendar going forward is non-negotiable: AGM by 30 September, AOC-4 and MGT-7 filed on schedule, DIR-3 KYC completed annually, and a full annual audit of every company where you hold a directorship. One default in one company is all it takes to trigger director disqualification India across your entire portfolio. Structure your compliance so it never comes to that.

📎 Authoritative Sources

- → MCA — Ministry of Corporate Affairs Official Portal

- → MCA — Disqualified Directors List under Section 164(2)(a)

- → MCA General Circular 01/2026 — CCFS 2026 (24 February 2026)

- → Companies Act 2013 — Section 164 (Disqualifications for Appointment of Director)

- → Companies Act 2013 — Section 252 (Restoration of Name)

- → NCLT — National Company Law Tribunal (Restoration Petitions)