Compliance Calendar for New Private Limited Company — Complete 2026 Guide: Never Miss a Deadline

Every essential deadline, statutory form, and penalty in one place — the complete ROC compliance checklist for any Private Limited Company incorporated on or after 1 April 2026.

First Board Meeting

+ Auditor Deadline

INC-20A Filing

Deadline

INC-20A

Non-Filing Penalty

AOC-4 / MGT-7

Late Fee (no cap)

- First Board Meeting within 30 days of incorporation: Directors must submit Form DIR-8 (non-disqualification) and Form MBP-1 (disclosure of interest) at this meeting. The first auditor must be appointed under Section 139(6) at the same meeting or within 30 days of incorporation.

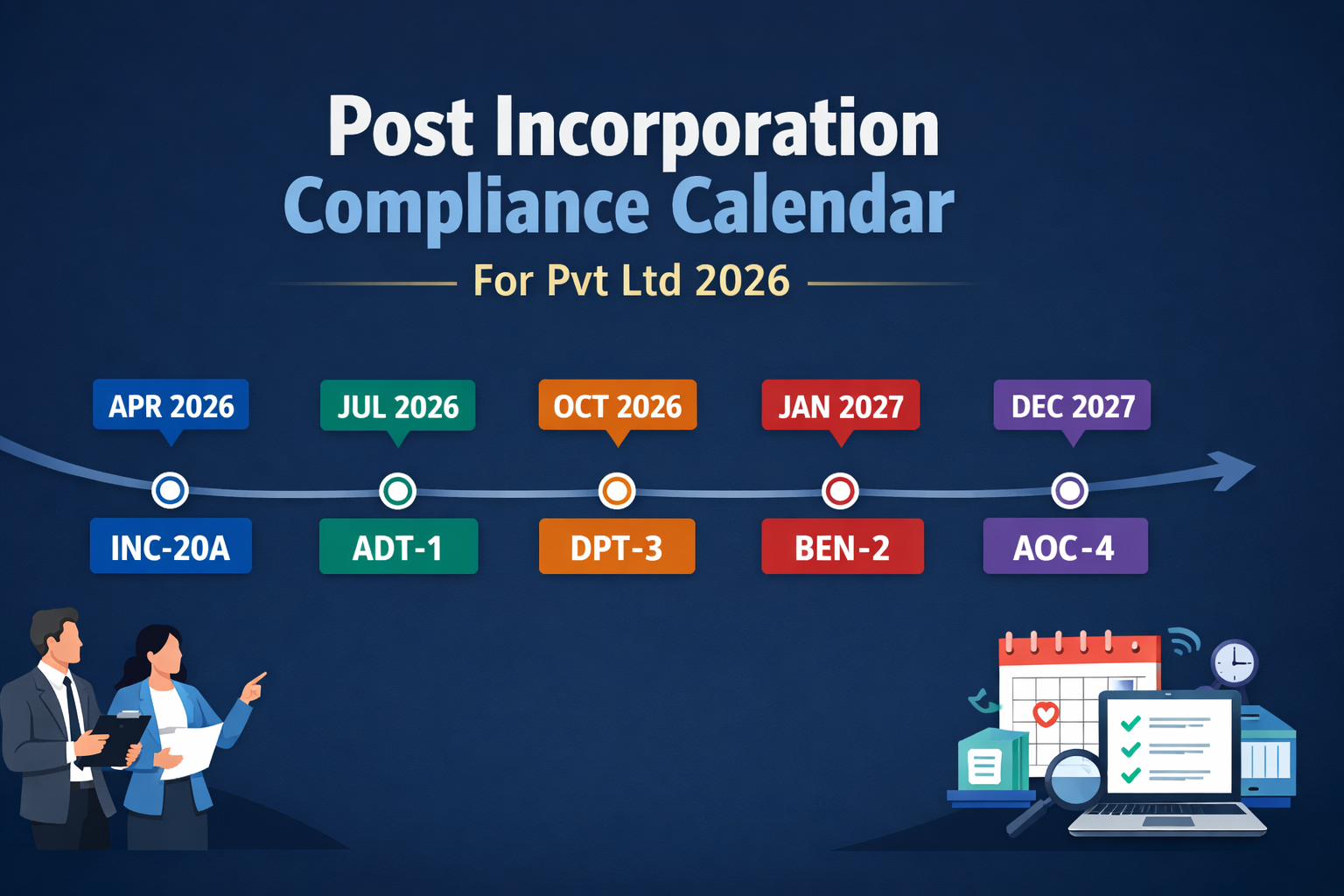

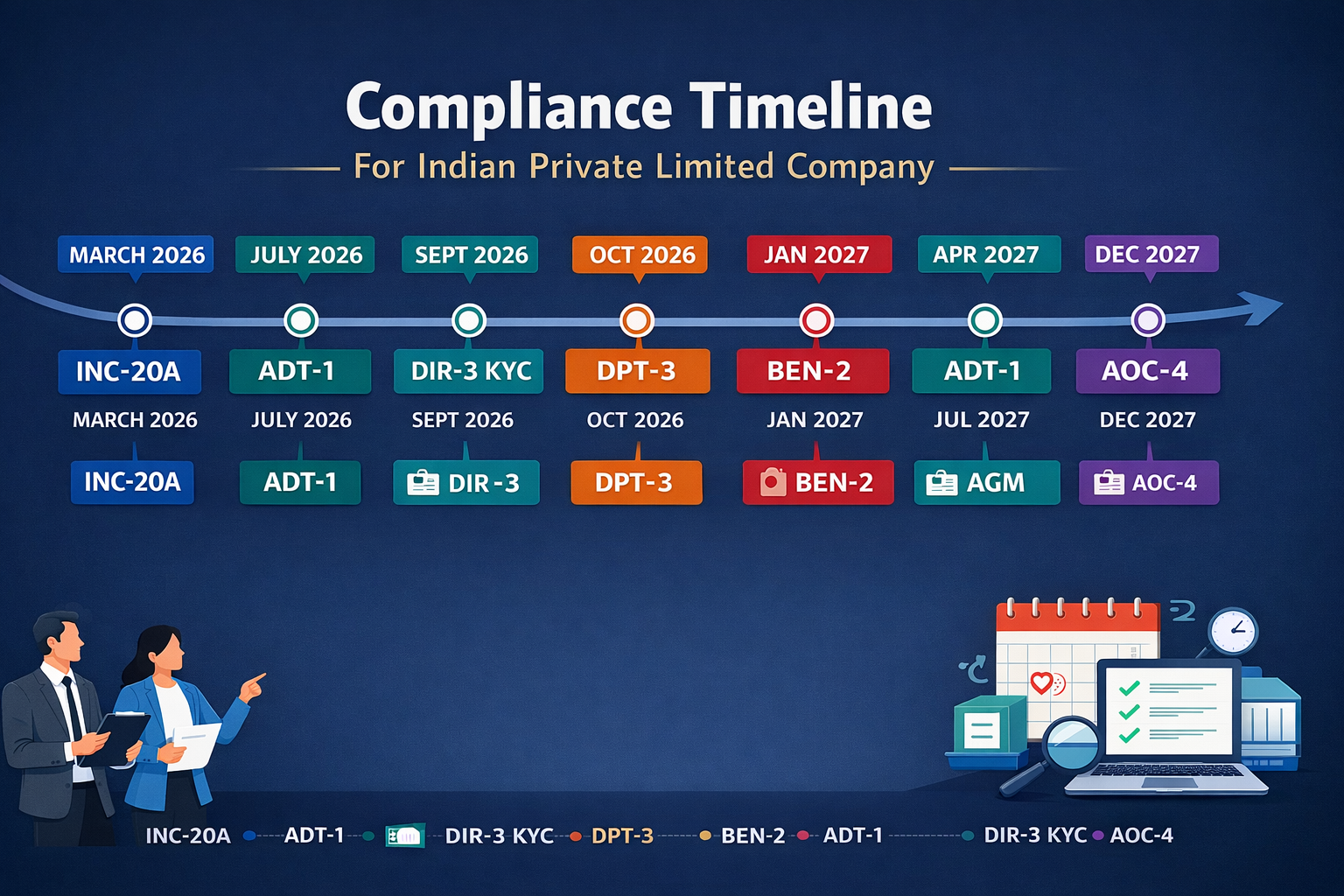

- INC-20A within 180 days of incorporation: The Declaration of Commencement of Business is the legal gateway to starting operations. No business activity, borrowing, or revenue transaction is permitted before this form is acknowledged by the ROC. Non-filing penalty: ₹50,000 on the company. File at mca.gov.in.

- Share certificates within 60 days of incorporation: Under Section 56(4)(a), certificates must be issued to all subscribers within 60 days. Non-small Private Limited Companies must issue shares in dematerialised (demat) form — physical certificates are not permitted for this category.

- DPT-3 by 30 June every year: This annual return of deposits and exempted deposits — including director loans and inter-corporate borrowings — is due by 30 June for the financial year ending 31 March. It is among the most frequently missed filings by newly incorporated companies.

- First AGM by 31 December of the year following the first financial year-end: For companies with a first financial year ending 31 March 2027, the AGM must be held by 31 December 2027. AOC-4 follows within 30 days of the AGM; MGT-7/7A within 60 days. No extension is available for the first AGM.

Post Incorporation Compliance Calendar for Private Limited Company — this is not a year-end task list. It is a continuous, legally binding obligation framework that begins on the day the Certificate of Incorporation is issued, not when the first invoice is raised or the first employee joins.

1 Financial Year Framework — The Foundation of Your Post Incorporation Compliance Calendar

Every annual compliance deadline in the Post Incorporation Compliance Calendar for Private Limited Company flows from one fixed anchor: the end of the first financial year. Under Section 2(41) of the Companies Act, 2013, every company’s financial year must end on 31 March. For a company incorporated on or after 1 April 2026, the first financial year runs from the date of incorporation to 31 March 2027. All annual filing deadlines — AGM, AOC-4, MGT-7, DPT-3 — are computed from this 31 March 2027 year-end.

2 Compliance Calendar for New Private Limited Company — Phase-by-Phase Deadlines

The following Post Incorporation Compliance Calendar for Private Limited Company covers every statutory obligation from the date of incorporation through the first full compliance cycle. Deadlines are expressed as days from incorporation or fixed annual dates so this calendar applies to every Private Limited Company regardless of their specific date of incorporation.

- Form DIR-8 (Non-Disqualification Declaration): Every director must submit a written declaration under Section 164(2) confirming they are not disqualified from holding a directorship. DIR-8 is retained at the registered office — not filed with MCA. Failure to submit: ₹1,00,000 penalty per director.

- Form MBP-1 (Disclosure of Interest): Every director must disclose their interest in other companies, firms, or entities under Section 184(1). MBP-1 must be renewed at the first Board Meeting of every financial year. Retained internally — not filed with MCA. Failure to disclose: ₹1,00,000 penalty per director.

- Appoint the First Auditor under Section 139(6). The auditor holds office until the conclusion of the first AGM.

- Authorise bank account signatories for the company’s current account.

- Authorise INC-20A filing once share subscription money is received.

- Fix accounting policies and confirm the financial year end (31 March).

INC-20A is the legal gateway to commencing business. A Private Limited Company cannot commence any business operations, exercise borrowing powers, or enter into revenue-generating contracts until Form INC-20A is filed and the ROC acknowledges it. Section 10A of the Companies Act, 2013 makes this an absolute statutory bar. File INC-20A as soon as share capital is received in the bank — do not wait until the 180-day deadline.

- A bank statement or bank certificate confirming receipt of the full share subscription amount from every subscriber to the MOA.

- Registered office address proof — a utility bill not older than 2 months, and a NoC from the property owner if the premises are not owned by the company (if not already confirmed via SPICe+).

- For regulated businesses (e.g., NBFCs require RBI approval, insurance companies require IRDAI approval) — a copy of the relevant regulatory licence or approval.

Penalties for INC-20A non-filing under Section 10A(2): Company — ₹50,000. Each director in default — ₹1,000 per day, subject to a maximum of ₹1,00,000 per director. Continued non-compliance beyond 180 days empowers the ROC to initiate strike-off proceedings under Section 248 of the Companies Act, 2013. Any business conducted before INC-20A is acknowledged renders directors personally liable for debts incurred during that period.

- Adoption of audited financial statements for FY 2026-27 (Balance Sheet, P&L, Directors’ Report, Auditor’s Report).

- Appointment or ratification of auditor for a 5-year term, followed by ADT-1 filing within 15 days of the AGM.

- Declaration of dividend (if any).

- Appointment of directors liable to retire by rotation (if applicable).

Important — OPC vs Private Limited Company: Under Section 96(1) of the Companies Act, 2013, One Person Companies (OPCs) are exempt from holding an Annual General Meeting. This exemption is exclusive to OPCs. Private Limited Companies — regardless of the number of shareholders or size — are required to hold the AGM within the prescribed timeline every year.

3 Complete ROC Compliance Checklist for Private Limited Company — Master Reference Table (FY 2026-27)

The following master table is your complete Post Incorporation Compliance Calendar for Private Limited Company, with relative deadlines, forms, and penalty references for every obligation. All deadlines marked “from incorporation” apply from your company’s specific date of incorporation.

| Compliance | Form | Deadline | Penalty for Default |

|---|---|---|---|

| Display Company Name and CIN | — (operational) | From Day 1 of incorporation | ₹1,000/day on company and officer |

| Open Company Bank Account | — (operational) | Immediately — prerequisite for INC-20A | INC-20A cannot be filed without bank statement |

| Intimation of Registered Office (if not filed at SPICe+) | INC-22 (ROC) | Within 30 days of incorporation | ₹1,000/day up to ₹1,00,000 |

| First Board Meeting | — (internal) | Within 30 days of incorporation | ₹25,000 company; ₹5,000 per director |

| DIR-8 (Non-Disqualification) | DIR-8 (retained at office) | At first Board Meeting (within 30 days) | ₹1,00,000 per director (Section 164) |

| MBP-1 (Disclosure of Interest) | MBP-1 (retained at office) | At first Board Meeting; renewed annually | ₹1,00,000 per director (Section 184) |

| Appointment of First Auditor | Board Resolution | Within 30 days of incorporation | Members must appoint at EGM within 90 days if Board fails |

| ADT-1 (Auditor Intimation) | ADT-1 (ROC) | Within 15 days of auditor appointment (effectively within 45 days of incorporation) | ₹300/day additional late filing fee |

| Share Certificate Issuance | Physical / Demat | Within 60 days of incorporation | ₹25,000 company; ₹5,000/day continuing default |

| BEN-1 / BEN-2 (Significant Beneficial Owner) | BEN-2 (ROC) | Within 30 days of receiving BEN-1 (if applicable) | Penalty under Section 90 on company and SBO |

| INC-20A (Commencement of Business) | INC-20A (ROC) | Within 180 days of incorporation | ₹50,000 company; ₹1,000/day per director (max ₹1 lakh) |

| DPT-3 (Return of Deposits / Loans) | DPT-3 (ROC) | By 30 June every year (for FY ending 31 March) | Up to ₹10 crore or 2× deposit amount |

| DIR-3 KYC (All Directors) | DIR-3 KYC / KYC-Web | By 30 September every year | ₹5,000 fixed; DIN deactivated until filed |

| MSME-1 — April to September period | MSME-1 (ROC) | By 31 October every year (if applicable) | ₹20,000 company; daily fines on directors |

| ITR-6 (Income Tax Return) | ITR-6 | By 31 October every year (for companies under audit) | ₹10,000 late fee; interest under Sections 234B & 234C |

| First AGM | — (meeting) | By 31 December 2027 (9 months from 31 March 2027) | ₹1,00,000 company; ₹5,000/day continuing default |

| ADT-1 (Post-AGM Auditor Ratification) | ADT-1 (ROC) | Within 15 days of AGM | ₹300/day additional late filing fee |

| AOC-4 (Financial Statements) | AOC-4 (ROC) | Within 30 days of AGM | ₹100/day — no maximum cap |

| MGT-7 / MGT-7A (Annual Return) | MGT-7 or MGT-7A | Within 60 days of AGM | ₹100/day — no maximum cap |

| MSME-1 — October to March period | MSME-1 (ROC) | By 30 April every year (if applicable) | ₹20,000 company; daily fines on directors |

4 What Applies to a Private Limited Company — INC-20A, AGM, AOC-4, MGT-7 Applicability Overview

The tables below map every post-incorporation and annual compliance to both categories of Private Limited Company — small and non-small. This covers the INC-20A filing deadline for Private Limited Company, MGT-7 and AOC-4 filing deadlines 2026, AGM requirements, BEN-2, and all threshold-based obligations — aligned with the Companies Act, 2013 and current MCA/ROC practice as of January 2026.

Section A — Post-Incorporation Compliance

| Compliance Requirement | Small Pvt Ltd (Capital ≤ ₹4 Cr & Turnover ≤ ₹40 Cr) |

Non-Small Pvt Ltd (Above either threshold) |

Statutory Basis |

|---|---|---|---|

| Intimation of Registered Office (INC-22) | ✓ If not filed at incorporation | ✓ If not filed at incorporation | Section 12 — within 30 days |

| Appointment of First Auditor | ✓ Mandatory | ✓ Mandatory | Section 139(6) — within 30 days |

| Declaration of Commencement of Business (INC-20A) | ✓ Mandatory | ✓ Mandatory | Section 10A — within 180 days |

| Appointment of Company Secretary (whole-time) | ✗ Not required below ₹10 Cr paid-up capital | ✓ Mandatory if paid-up capital ≥ ₹10 Cr | Section 203 — MR-1 within 60 days of appointment |

| Significant Beneficial Owner (BEN-1 / BEN-2) | ✓ If indirect SBO exists | ✓ If indirect SBO exists | Section 90 — within 30 days of BEN-1 receipt |

| Share Certificate / Dematerialisation | ✓ Physical certificates permitted | ✓ Demat mandatory — Rule 9B | Section 56(4)(a) — within 60 days |

Section B — Annual Compliance

| Compliance Requirement | Small Pvt Ltd | Non-Small Pvt Ltd | Statutory Basis |

|---|---|---|---|

| Annual General Meeting (AGM) | ✓ Mandatory OPCs are exempt under Section 96(1) |

✓ Mandatory | Section 96 — 9 months from financial year-end |

| Filing of Annual Return | ✓ MGT-7A (simplified, self-certified) | ✓ MGT-7 (CS certification mandatory) | Section 92 — within 60 days of AGM |

| Filing of Financial Statements | ✓ AOC-4 (no Cash Flow Statement) | ✓ AOC-4 (including Cash Flow Statement) | Section 137 — within 30 days of AGM |

| Filing of DPT-3 | ✓ If any loans / exempted deposits exist | ✓ If any loans / exempted deposits exist | Rule 16 — by 30 June annually |

| Director KYC (DIR-3 KYC) | ✓ All DIN holders | ✓ All DIN holders | Rule 12A — by 30 September annually |

| Significant Beneficial Owner Filing (BEN-2) | ✓ If SBO exists | ✓ If SBO exists | Section 90 — event-based, within 30 days |

| Board Meetings per year | ✓ Minimum 2 (one per half-year; 90 days apart) | ✓ Minimum 4 (max 120 days between consecutive) | Section 173 |

| Secretarial Audit (MR-3) | ✗ Not applicable below threshold | ✓ If paid-up capital ≥ ₹50 Cr or turnover ≥ ₹250 Cr | Section 204 read with Rule 9 |

| Board Committees (Audit / NRC) | ✗ Generally not applicable | ✓ Threshold-based — primarily for listed and large public companies | Sections 177 & 178 |

| Quarterly Filings | ✗ Not applicable (unlisted) | ✗ Not applicable (unlisted) | Applicable only to listed companies under SEBI (LODR) |

Small company status must be re-evaluated at every 31 March year-end. A company that qualifies as small at incorporation may exceed either threshold during FY 2026-27. If it does, the higher-compliance regime — MGT-7 (CS certified), Cash Flow Statement in AOC-4, mandatory demat shares, and four Board Meetings — applies from the following year. Misclassifying as a small company when the thresholds have been crossed constitutes a default under the Companies Act, 2013.

5 Ongoing ROC Compliance Checklist for Private Limited Company — Board Meetings and Statutory Registers

Beyond the INC-20A filing deadline and the annual ROC filings, the Companies Act, 2013 requires all statutory registers to be maintained at the registered office from Day 1 of incorporation. This is a continuous part of the ROC compliance checklist for Private Limited Company 2026 — not a filing that happens once a year. All registers must be maintained and available for inspection at all times.

- ✓Register of Members (MGT-1): Names, addresses, shareholding details, and folio numbers of all members. Must be updated within 7 days of any change in membership or shareholding structure.

- ✓Register of Directors and KMP (MBP-4): Details of all directors and Key Managerial Personnel — DIN, PAN, date of appointment, residential address, and other directorships held. Must be updated within 30 days of any change.

- ✓Register of Charges (CHG-7): Details of all charges created on the company’s assets — mortgages, hypothecations, pledges, and other encumbrances — from the date the charge is created.

- ✓Register of Loans, Investments, Guarantees and Security (MBP-2): Mandatory under Section 186. Records all inter-corporate loans, investments made, guarantees given, and security provided by the company — including terms and purpose of each transaction.

- ✓Register of Contracts with Related Parties (MBP-4): Records all related party contracts and arrangements under Sections 184 and 188, including the nature of the transaction and whether Board or shareholder approval was obtained.

- ✓Minutes Books: Separate bound volumes for Board Meeting minutes and General Meeting minutes. The Chairman must sign the minutes within 30 days of each meeting. Minutes must be retained permanently and cannot be destroyed.

- !Register of Significant Beneficial Owners (BEN-3): Internal register of all SBO declarations received via Form BEN-1, maintained under Section 90(9). Must be available for inspection at the registered office at all times.

- !Register of Share Transfers: Records every transfer instrument (SH-4) and the corresponding update to the Register of Members. Must be updated within 60 days of presentation of the transfer instrument.

6 Event-Based Filings — DIR-12, PAS-3, CHG-1 and More for Private Limited Company Compliance After Incorporation

Several obligations within the Private Limited Company compliance after incorporation framework are not calendar-driven but are triggered by specific corporate events. These must be filed within the prescribed window from the date of the event — delays attract the same per-day penalty structure as annual filings like AOC-4 and MGT-7.

| Corporate Event | Form | Filing Window |

|---|---|---|

| Appointment / Resignation of Director | DIR-12 | Within 30 days of the event |

| New Allotment of Shares (capital raise) | PAS-3 | Within 30 days of allotment |

| Transfer of Shares | SH-4 + Register update | Within 60 days of presentation of transfer instrument |

| Special / Ordinary Resolution (Section 117) | MGT-14 | Within 30 days of passing the resolution |

| Change of Registered Office (same city) | INC-22 | Within 15 days of change |

| Change of Registered Office (different city / state) | INC-23 + INC-28 | ROC / NCLT approval required prior to change |

| Creation of Charge (bank loan, mortgage) | CHG-1 | Within 30 days (extendable to 60 days with additional fee; up to 120 days with Registrar approval) |

| Satisfaction / Release of Charge | CHG-4 | Within 30 days of satisfaction |

| Appointment of KMP (CEO, CFO, CS) | MR-1 | Within 60 days of appointment (where mandatory) |

| Alteration of MOA / AOA | MGT-14 + INC-27 | Within 30 days of special resolution |

| Change in Company Name | INC-24 + INC-25 | After ROC name approval via RUN / SPICe+ |

7 Tax and Regulatory Compliance After Incorporation — GST, TDS, Advance Tax, PF and More

The MCA compliance layer runs concurrently with tax and regulatory obligations under the Income Tax Act, Goods and Services Tax Act, and sector-specific statutes. These obligations are equally important parts of the Post Incorporation Compliance Calendar for Private Limited Company and represent the complete picture of Private Limited Company compliance after incorporation.

- ✓GST Registration: Mandatory when aggregate turnover exceeds ₹40 lakh (goods) or ₹20 lakh (services) per year. Voluntary registration is advisable for B2B operations to enable Input Tax Credit. Monthly filings: GSTR-1 (outward supplies) and GSTR-3B (tax payment summary). Quarterly QRMP scheme is available for turnover below ₹5 crore. Register at gst.gov.in.

- ✓TDS Deduction and Remittance: Applicable when the company makes payments above statutory thresholds — salary, rent, professional fees, contractor payments, interest. TDS must be deducted and deposited by the 7th of the following month. Quarterly TDS returns (Form 24Q for salary; Form 26Q for non-salary) must be filed. Non-deduction or non-deposit attracts interest at 1–1.5% per month plus a penalty equal to the tax not deducted.

- ✓Advance Tax: If total tax liability for the financial year exceeds ₹10,000, advance tax must be paid in four instalments — by 15 June (15%), 15 September (45%), 15 December (75%), and 15 March (100%). Short-payment or non-payment attracts interest under Sections 234B and 234C of the Income Tax Act, 1961. Verify at incometax.gov.in.

- !Provident Fund (PF) Registration: Mandatory once the company has 20 or more employees. Monthly ECR (Electronic Challan cum Return) and contributions must be remitted by the 15th of the following month. Register at epfindia.gov.in.

- !ESIC Registration: Mandatory once the company has 10 or more employees (in most states) with wages up to ₹21,000 per month. Monthly contribution remittance and half-yearly return filing are required.

- !Professional Tax (State-Specific): Applicable in Maharashtra, Karnataka, Tamil Nadu, West Bengal, and several other states. Registration requirements and payment cycles vary by state. Non-compliance attracts state-level penalties.

- !DPIIT Startup India Recognition (if eligible): Companies incorporated within the last 10 years, with annual turnover not exceeding ₹100 crore, working towards innovation or a scalable business model, may apply for DPIIT recognition. Benefits include tax exemption under Section 80-IAC, self-certification under labour laws, and fast-track IP filing. Apply at startupindia.gov.in.

- ₹FLA Return (RBI) — if foreign investment received: Companies that have received FDI or made Overseas Direct Investment (ODI) must file the Foreign Liabilities and Assets Annual Return with the RBI by 15 July every year. This is filed on the RBI’s FIRMS portal — entirely separate from all MCA filings. Verify at rbi.org.in.

8 Penalties for Non-Compliance — Why Private Limited Company Annual Compliance Requirements Cannot Be Ignored

Understanding the Private Limited Company annual compliance requirements India mandates is critical — the Companies Act, 2013 operates on a per-day penalty structure for most defaults with no maximum cap on the most critical filings. For a newly incorporated Private Limited Company, these are the three highest-risk consequences in the first two years.

Zero business activity is not an exemption from any filing. A company with no transactions, no revenue, and no employees must still file INC-20A, DPT-3, AOC-4 (nil balance sheet), MGT-7/7A, and DIR-3 KYC for all directors. The obligation arises from the company’s registered existence under the Companies Act, 2013 — not from its operational status. This is one of the most expensive compliance misconceptions among first-time founders.

Stay on Top of Your Post Incorporation Compliance — Never Miss a Deadline

Our team manages the complete post incorporation compliance calendar for Private Limited Companies — INC-20A, ADT-1, BEN-2, DPT-3, MSME-1, annual ROC filings, GST returns, and TDS. We track every deadline so your focus stays on the business.

Get a Free Consultation → View ROC Compliance Services9 Frequently Asked Questions — INC-20A Filing Deadline, AGM, AOC-4 and MGT-7 for Private Limited Company

10 Conclusion — Your Post Incorporation Compliance Calendar for Private Limited Company Starts on Day One

The Post Incorporation Compliance Calendar for Private Limited Company is not a year-end checklist — it is a continuous obligation framework that starts the moment the Certificate of Incorporation is issued. The first Board Meeting within 30 days, Form ADT-1 within 15 days of auditor appointment, share certificates within 60 days, and Form INC-20A within 180 days — each is a statutory deadline with daily penalties, director disqualification exposure, and ROC-initiated strike-off risk if missed. The annual cycle then adds DIR-3 KYC by 30 September, DPT-3 by 30 June, the first AGM by 31 December 2027, and AOC-4 and MGT-7/7A within 30 and 60 days of the AGM respectively.

Two distinctions materially affect your specific compliance burden. First, the small company classification — if your paid-up capital stays below ₹4 crore and turnover below ₹40 crore at the 31 March year-end, you file MGT-7A (not MGT-7) and hold two Board Meetings instead of four. Second, the demat share requirement — non-small Private Limited Companies must issue shares in dematerialised form only, which requires an ISIN and an RTA to be in place before the 60-day share certificate deadline arrives. Both determinations must be made at every financial year-end based on actual audited figures.

The most effective approach to Private Limited Company compliance after incorporation is to appoint a qualified Chartered Accountant and a Company Secretary from Day 1, map every relative deadline into a shared compliance calendar from the date of incorporation, and treat this Post Incorporation Compliance Calendar for Private Limited Company as a founding function — not an afterthought. A single missed MCA filing can block a bank loan, freeze a funding due diligence process, or result in a director losing the ability to sign any company document across all their directorships in India.

📎 Authoritative Sources

- → MCA — Companies Act, 2013 (Sections 10A, 56, 90, 92, 96, 137, 139, 164, 173, 184, 203, 248)

- → MCA — Company Forms Portal (INC-20A, INC-22, ADT-1, DPT-3, BEN-2, MSME-1, DIR-3 KYC, AOC-4, MGT-7, MGT-7A, PAS-3, CHG-1, DIR-12)

- → MCA — Companies (Incorporation) Rules, 2014 (Rule 23A — INC-20A) and Companies (Acceptance of Deposits) Rules, 2014 (Rule 16 — DPT-3)

- → Income Tax India — ITR-6 Filing Portal and Advance Tax Schedule

- → GST Portal — Registration, GSTR-1 and GSTR-3B Return Filing

- → Startup India — DPIIT Recognition and Section 80-IAC Tax Exemption Eligibility

- → Reserve Bank of India — FLA Annual Return (FIRMS Portal) for FDI and ODI Reporting