GST Registration Turnover Limit 2026: Is Registration Mandatory?

Let us cut through the noise. Whether you are bootstrapping a private limited company or steering a legacy manufacturing enterprise, operating under the radar of the Goods and Services Tax (GST) framework is not a strategy; it is a fatal legal liability. Ignorance of the GST Turnover Limit will not shield you from the rigorous enforcement of the Central Board of Indirect Taxes and Customs (CBIC). If your financial aggregate breaches the statutory threshold, the law dictates immediate compliance, offering zero room for subjective interpretation.

At VALIDRAFT, we witness businesses routinely face debilitating penalties under Section 122 of the CGST Act simply because they miscalculated their aggregate turnover or misunderstood state-specific variations. This unfiltered, legally grounded guide will decode the precise GST Registration Limit for goods and services in 2026, outline the scenarios where the threshold drops to absolute zero, and provide you with the exact regulatory clarity required to safeguard your corporate entity.

The Statutory Baseline: Section 22 of the CGST Act

The foundation of the GST Threshold Limit is codified within Section 22(1) of the Central Goods and Services Tax (CGST) Act, 2017. The law mandates that every supplier shall be liable to be registered in the State or Union territory from where they make a taxable supply if their aggregate turnover in a financial year exceeds the defined limits. However, the exact numbers fluctuate based on two critical variables: the nature of your supply (Goods vs. Services) and your geographical jurisdiction.

Here is the absolute, unembellished legal breakdown for the financial year 2026:

| Jurisdiction / State Category | GST Registration Limit (Exclusive Supply of Goods) | GST Registration Limit (Supply of Services or Both) |

|---|---|---|

| Normal Category States (e.g., Maharashtra, Delhi, Karnataka, Gujarat, Tamil Nadu, Uttar Pradesh) |

₹40 Lakhs | ₹20 Lakhs |

| Special Category States (Tier 1) (Manipur, Mizoram, Nagaland, Tripura) |

₹10 Lakhs | ₹10 Lakhs |

| Special Category States (Tier 2) (Arunachal Pradesh, Meghalaya, Sikkim, Uttarakhand, Puducherry, Telangana) |

₹20 Lakhs | ₹20 Lakhs |

Decoding the GST Turnover Limit : The Trap of Miscalculation

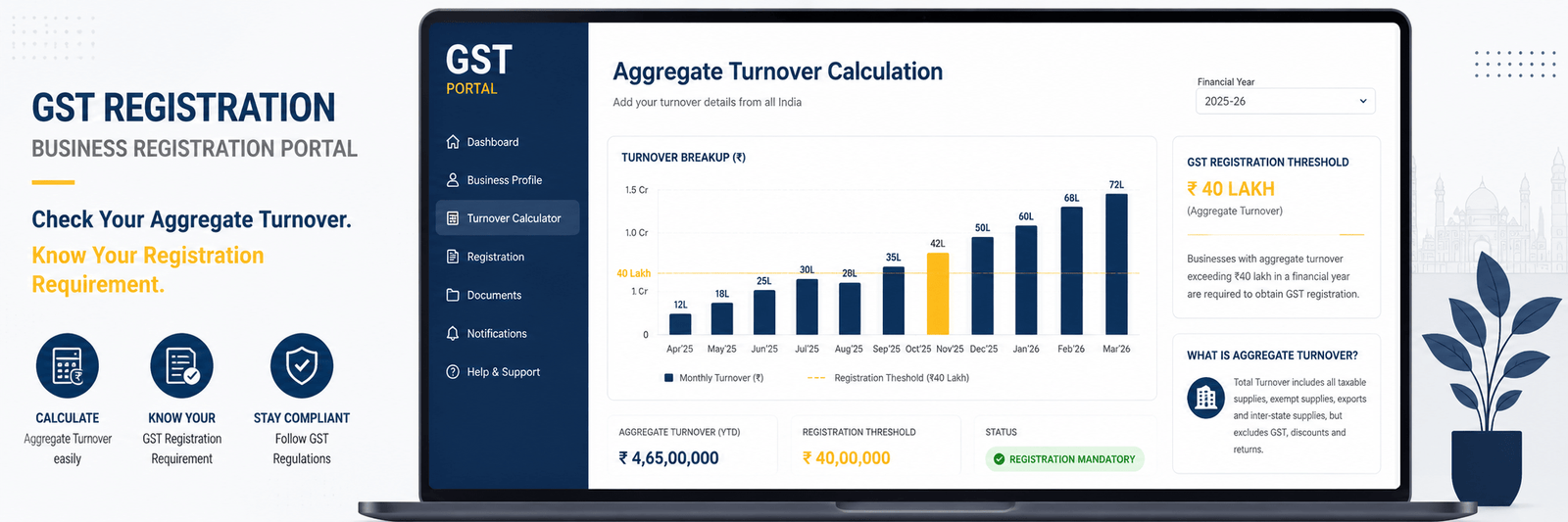

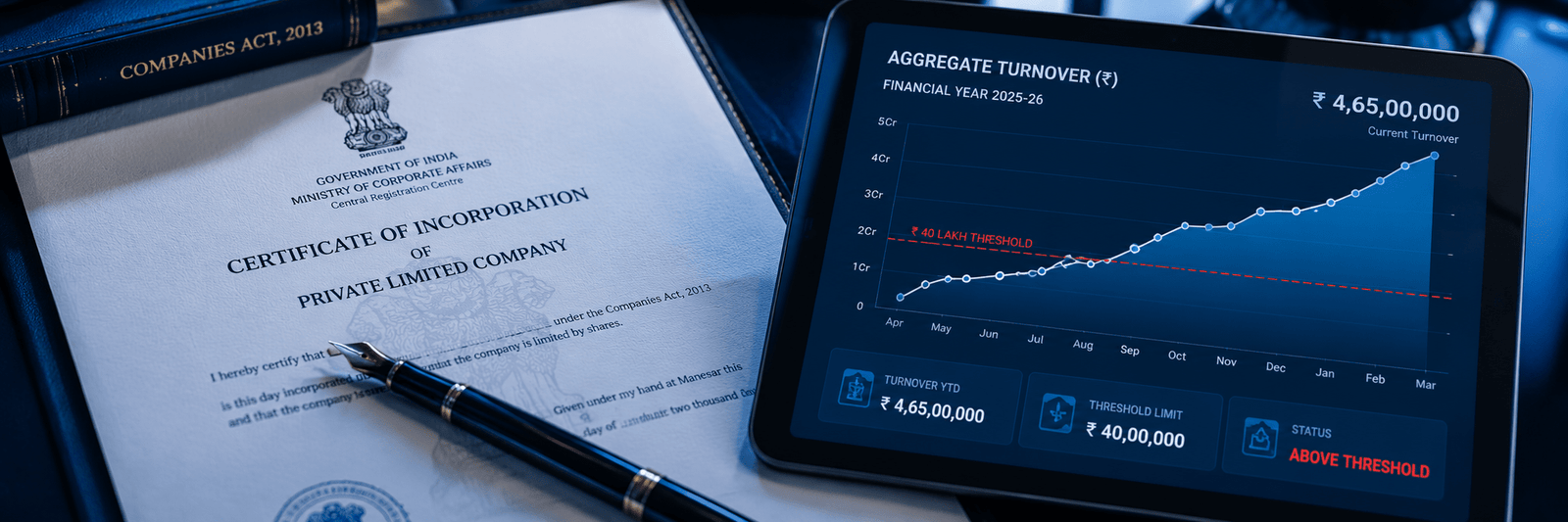

A fatal flaw made by many unrepresented business owners is equating “taxable sales” with “aggregate turnover.” The calculation for the GST Turnover Limit is comprehensively defined under Section 2(6) of the CGST Act. The law requires a Pan-India computation across all branches operating under a single Permanent Account Number (PAN).

To accurately determine if you have crossed the GST Registration Limit, your aggregate turnover MUST include:

- Taxable Supplies: The core revenue generated from standard business operations.

- Exempt Supplies: Goods or services that attract a nil rate of tax or are wholly exempt (e.g., certain agricultural produce or healthcare services).

- Exports: Zero-rated supplies of goods or services outside India.

- Inter-State Transfers: Stock transfers between distinct persons (e.g., your Delhi factory sending goods to your Mumbai warehouse).

If the sum of these elements crosses your designated GST Threshold Limit, you are legally obligated to apply for registration in Form GST REG-01 via the Official GST Portal within 30 days of becoming liable.

Section 24: When the GST Threshold Limit is Zero

Threshold limits offer a false sense of security for modern, digitized business models. Under Section 24 of the CGST Act, the concept of a GST Turnover Limit is entirely bypassed. For specific categories, mandatory registration is triggered the moment the first transaction occurs, regardless of the revenue amount. If you fall into any of the following brackets, your GST Registration Limit is effectively ₹0:

- Inter-State Supply of Goods: Selling physical products across state borders demands immediate registration. (Note: Inter-state service providers are protected up to the ₹20 Lakh limit under Notification No. 10/2017-Integrated Tax).

- E-Commerce Operations: Supplying goods through aggregators like Amazon, Flipkart, or Swiggy mandates day-one registration.

- Reverse Charge Mechanism (RCM): Persons required to pay tax under RCM (e.g., businesses utilizing Goods Transport Agencies or unregistered advocates) must register.

- Casual & Non-Resident Taxable Persons: Temporary business operators displaying goods at exhibitions outside their home state.

- OIDAR Service Providers: Overseas entities providing digital data or cloud services to unregistered Indian consumers.

If you operate within these parameters and are relying on the standard GST Threshold Limit to avoid compliance, you are actively committing a tax offense.

GST Registration Eligibility Assessor (2026)

Use this strictly formulated legal tool to evaluate if your business has breached the mandatory GST Registration Limit.

The Legal Repercussions of Evading the GST Threshold Limit

Tax authorities do not issue polite reminders when you cross the GST Turnover Limit. Evasion—whether intentional or born of negligence—triggers severe punitive action under the CGST Act. The consequences of failing to secure a GSTIN upon breaching the GST Registration Limit include:

- Mandatory Penalties: Section 122(1) levies a penalty of ₹10,000 or 10% of the tax due, whichever is higher. For deliberate fraud, the penalty scales to 100% of the tax evaded.

- Asset Confiscation & Bank Attachments: Authorities hold the statutory right to freeze business bank accounts to recover dues.

- Denial of Input Tax Credit (ITC): Without a valid GST registration, you cannot claim ITC on the taxes paid on your purchases. This radically inflates your operating costs, placing you at a severe competitive disadvantage.

- Loss of Corporate Credibility: Premium B2B vendors and institutional clients mandate GST compliance. You cannot participate in government tenders, list on elite e-commerce platforms, or secure large corporate contracts without a GSTIN.

Final Verdict: Institutionalize Your Compliance with VALIDRAFT

The architecture of Indian taxation leaves no margin for error. Tracking your progression toward the GST Turnover Limit is not merely an accounting task; it is a critical aspect of corporate governance. Whether your operations are rooted in a special category state grappling with a ₹10 Lakh limit, or you are scaling a nationwide goods network subject to mandatory zero-limit thresholds, precision is non-negotiable.

Do not wait for a show-cause notice from the CBIC. If your business is approaching the GST Threshold Limit or if you are expanding into inter-state territories, you require elite legal structuring.