West Bengal E-Way Bill Registration & Compliance: The Complete Statutory Guide

In the framework of indirect taxation in India, logistics compliance is a critical point of operational risk management. For enterprises moving commercial stock within, into, or out of West Bengal, strict adherence to the electronic way bill (e-way bill) rules is non-negotiable. Missing state-specific mandates or miscalculating cross-border values can trigger immediate vehicle detention, severe financial penalties under Section 129 of the CGST Act, and major supply chain friction.

Understanding the intersections of local notifications and cross-border mandates is vital for legal and financial officers. Below is the verified operational playbook required to execute a flawless West Bengal E-Way Bill Registration, trigger the WB E-Way Bill Apply mechanisms, and manage cross-border transshipments securely.

The Cross-Border vs. Local Statutory Matrix

The requirement to generate an e-way bill is determined by the geographical borders crossed, the reason for the movement, and the consignment value under Section 15 of the CGST/WBGST Act, 2017. This value must include CGST, SGST, UTGST, or IGST, but explicitly excludes the value of exempt supplies when a mixed invoice is issued.

| Movement Typology | Consignment Threshold Limit | Statutory Conditions & Exemptions | Governing Provision |

|---|---|---|---|

| Cross-Border / Inter-State Supply | Exceeding ₹50,000 | Mandatory nationwide. Local state exemptions or higher limits cease to apply the moment a truck crosses the state boundary line. | Rule 138 of CGST Rules, 2017 |

| Intra-State Supply (West Bengal) | Exceeding ₹50,000 | Strict limit under Notification No. 02/2026-C.T./GST. Restores tight tracking on local commercial trades. | Notification No. 02/2026-C.T./GST |

| Intra-State Job Work | Fully Exempted | Explicitly excluded from the 2026 threshold reduction. Local movements for job work within West Bengal do not require an e-way bill. | Section 2(68) read with Notif. 02/2026 |

| Cross-Border Job Work | Mandatory at Zero Value | Strict zero-threshold rule. If goods are sent from West Bengal to a job worker in another state, an e-way bill is compulsory regardless of value. | Third Proviso to Rule 138(1) of CGST Rules |

Failing to monitor these limits leaves shipments exposed to penalties. Under Section 129, penalties can reach 200% of the tax payable on the transported goods, making real-time data verification mandatory.

Strict Platform Rules and System Frameworks

To execute the E-Way Bill Application Process without encountering structural validation errors, compliance teams must follow specific system constraints introduced to prevent tax evasion:

- The 180-Day Rule: The e-way bill portal blocks generations for any tax invoice, delivery challan, or bill of entry dated more than 180 days prior. Old or delayed shipments cannot be cleared retroactively.

- Universal 2FA Mandate: Accessing the portal requires mandatory Multi-Factor Authentication (MFA) to secure data integrity.

- Upcoming June 15, 2026 Protocol: The portal is introducing a mandatory requirement to capture the “Ship To GSTIN” explicitly for all complex Bill-To/Ship-To transactions, directly affecting multi-state cross-border assignments.

Step-by-Step Onboarding and Infrastructure Setup

- Access the official unified national logistics platform directly at ewaybillgst.gov.in. Do not utilize unverified third-party compliance scraping portals.

- Navigate to ‘Registration’ on the main landing navbar and select ‘E-Way Bill Registration’.

- Input your active 15-digit West Bengal GSTIN. The portal will initiate a secure API handshake to auto-populate your registered commercial details.

- Trigger and complete the OTP authentication sent to the mobile and email registered on the core GSTN database.

- Set up highly secure corporate access credentials to authorize your logistics team.

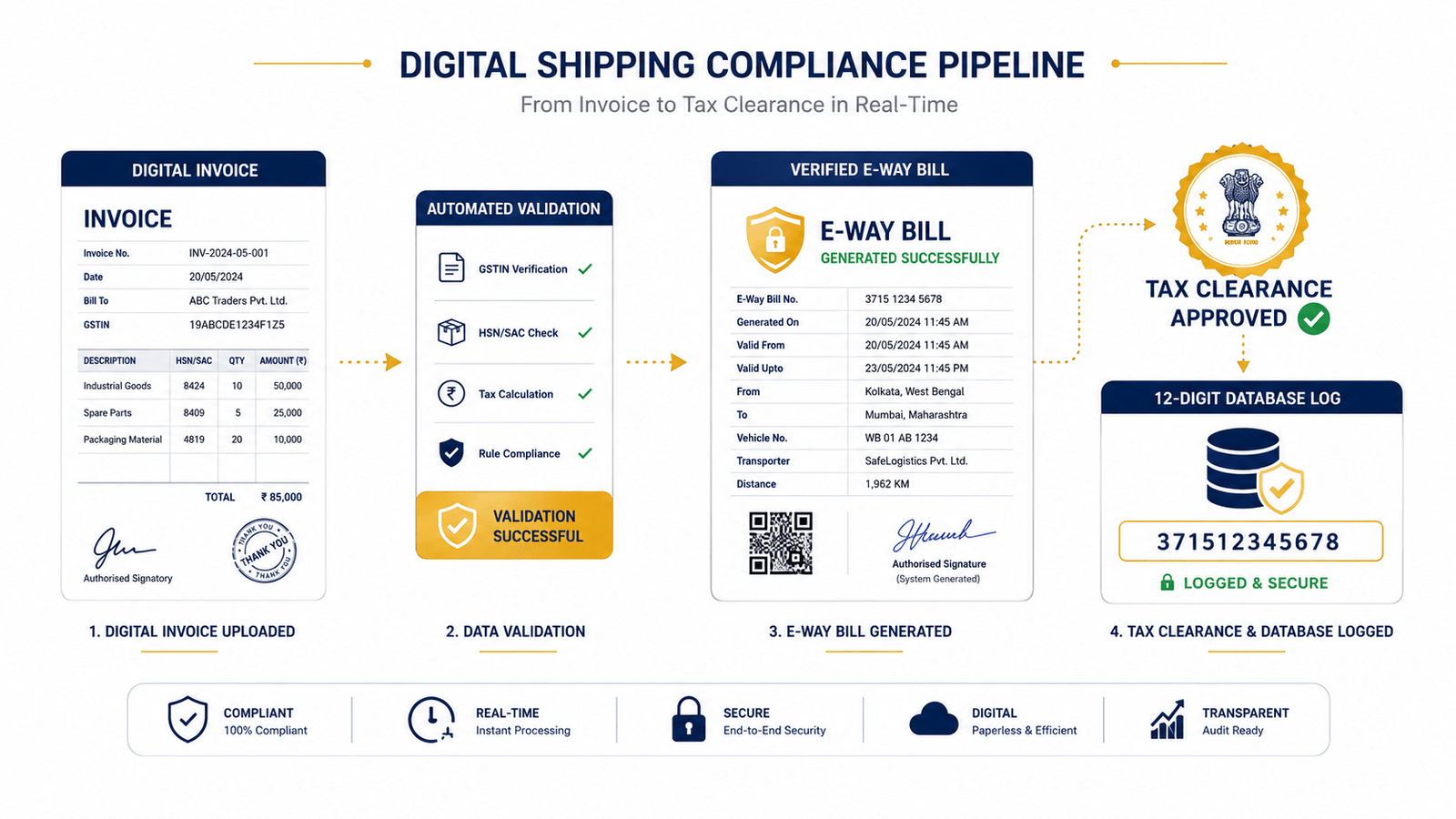

Operational Protocol: E-Way Bill Login & E-way Bill Check

With active portal credentials, your dispatch desk must initialize the WB E-Way Bill Apply sequence prior to any physical cargo leaving the warehouse platform. This document is split into Part A (document and tax metadata) and Part B (conveyance registration).

The Part B Distance Proviso: For local transport within West Bengal, if the distance from the consignor’s location to the transporter’s warehouse is less than 50 kilometers, updating Part B is legally optional. However, if the cross-border or local distance exceeds 50 kilometers, moving a vehicle without valid Part B information constitutes a severe compliance violation.

Daily Operational Compliance Flow

- Authentication: Securely log in through the main E-Way Bill Login panel using multi-factor credentials.

- Data Entry (Part A): Select ‘Generate New’. Input the required tax documentation, including mandatory Harmonized System of Nomenclature (HSN) codes.

- Vehicle Mapping (Part B): Provide the precise vehicle registration number or transporter document number to legally complete the document.

- The E-way Bill Check: Prior to final vehicle dispatch, gate supervisors must run an automated E-way Bill Check using the 12-digit number to verify that the validity period (1 day per 200 km for regular cargo) remains active.

West Bengal E-Way Bill Registration Compliance Checker

Use our interactive legal evaluator tool to determine if an upcoming commercial shipment requires a mandatory electronic way bill under current WBGST and CGST provisions. Adjust your parameters below for an immediate determination.

Insulating Your Supply Chain from Penalties

Leaving logistical compliance to manual checking or outdated information creates unnecessary legal exposure. Protecting your corporate cash flows from unexpected detentions requires structured workflows, regular internal compliance reviews, and automated verification protocols.

Insulate Your Corporate Logistics from Severe Tax Penalties

Protect your logistics network from costly transport delays and vehicle seizures. Validraft builds automated, legally compliant internal architectures aligned precisely with active CGST and WBGST mandates.

Consult Our Corporate Tax Counsel Now