GST Registration Process: Step-by-Step Guide for New Businesses in 2026

Operating a commercial enterprise without statutory registration when legally required invites severe financial penalties under Section 122 of the Central Goods and Services Tax (CGST) Act, 2017. As of 2026, the Goods and Services Tax Network (GSTN) has integrated advanced automated risk-profiling algorithms and strict localized biometric validation pipelines to counter systemic tax evasions. Consequently, executing an error-free GST Registration Process requires absolute adherence to precise regulatory updates, structural formatting timelines, and compliance procedures.

This statutory GST Registration Guide establishes the exact criteria, definitive structural phases, and mandatory post-approval mechanisms required to formalize your business entity securely online.

1. Statutory Thresholds and Liability Framework (2026 Metrics)

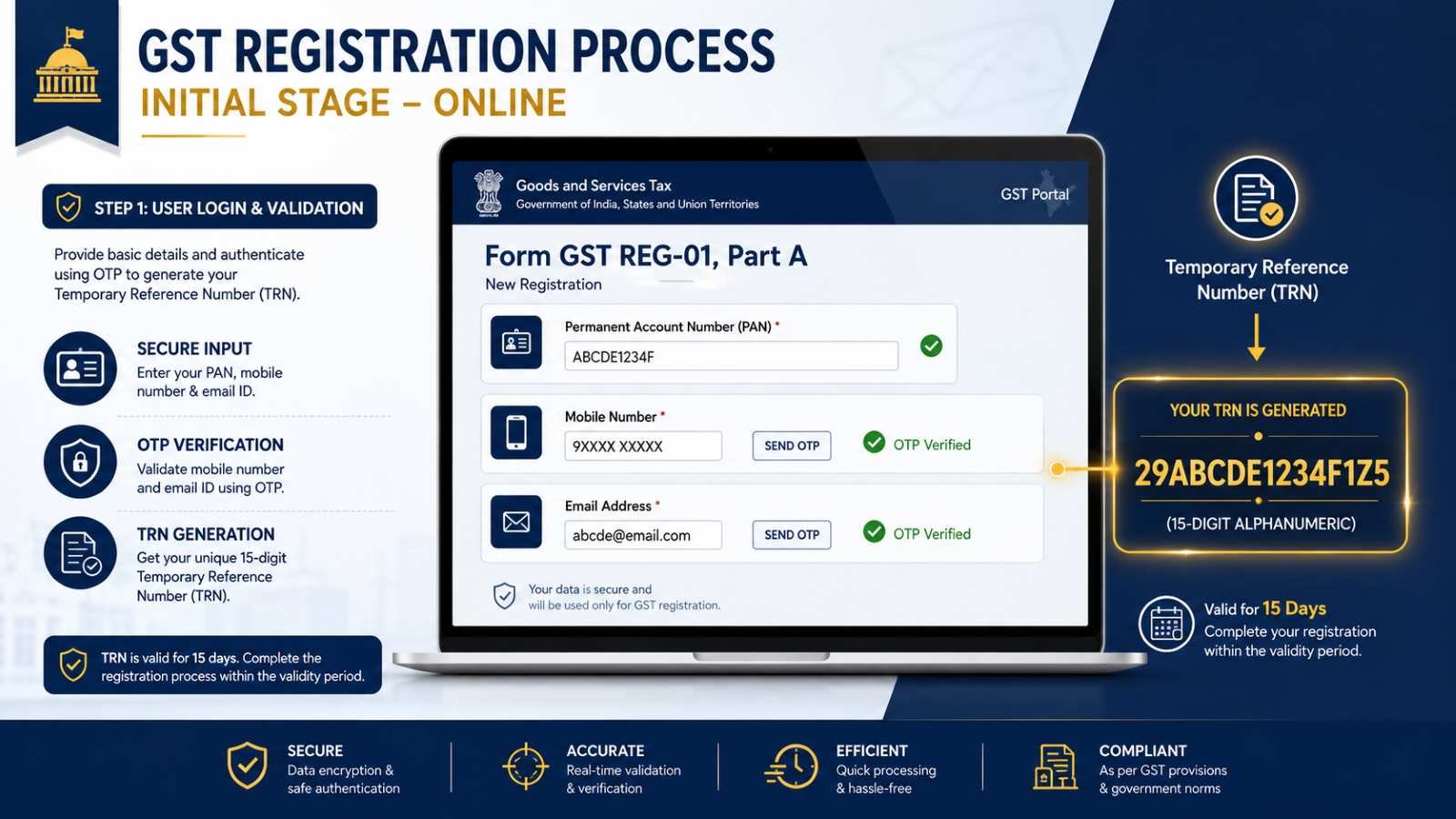

As illustrated in the interface of image_c273ce.png, evaluating dynamic parameters like core operations and jurisdictional boundaries is mandatory before launching your GST Registration Online application. Under Section 22, the statutory threshold limits are segregated into three strict legal classifications based on state-wise adjustments:

| Jurisdictional Category & Covered States | Exclusive Supply of Goods | Service Providers / Mixed Supplies |

|---|---|---|

| Group 1: Manipur, Mizoram, Nagaland, Tripura | ₹10 Lakhs Aggregate Turnover | ₹10 Lakhs Aggregate Turnover |

| Group 2: Arunachal Pradesh, Meghalaya, Sikkim, Uttarakhand, Puducherry, Telangana | ₹20 Lakhs Aggregate Turnover | ₹20 Lakhs Aggregate Turnover |

| Group 3: Rest of India (e.g., MH, DL, KA, WB, JK, AS, HP) | ₹40 Lakhs Aggregate Turnover | ₹20 Lakhs Aggregate Turnover |

Aggregate turnover is calculated on an all-India basis under the same PAN. It encompasses all taxable supplies, exempt supplies, exports of goods or services, and inter-state supplies, while excluding central tax, state tax, union territory tax, and integrated tax.

Absolute Overrides: Section 24 Compulsory Registration

The standard turnover thresholds are completely voided if your business triggers any provisions of Section 24. Registration is legally mandatory within 30 days from the inception of business activities, even if your total annual revenue is zero, for:

- Entities conducting inter-state taxable outward supplies of goods.

- Electronic Commerce Operators (ECO) required to collect tax at source under Section 52.

- Persons supplying goods or services through an ECO (subject to localized municipal relaxation rules).

- Persons liable to settle tax liabilities under the Reverse Charge Mechanism (RCM).

- Casual Taxable Persons (CTPs) and Non-Resident Taxable Persons (NRTPs) operating transient commercial ventures.

Statutory GST Eligibility & Threshold Evaluator

Execute a secure regulatory check to evaluate your business liability and establish your exact registration mandate under current provisions.

2. The End-to-End Online GST Registration Process

The contemporary digitized sequence on the Official GST Common Portal transitions through discrete programmatic gates. Any mismatch in structural metadata triggers automated rejections or immediate system-generated notices.

Phase 1: Temporary Reference Number (TRN) Generation

Initiate the initial digital filing sequence through Form GST REG-01, Part A. The applicant enters a valid Permanent Account Number (PAN), primary business email address, and an active mobile number. The system executes immediate electronic verification via dual One-Time Password (OTP) challenges. Upon successful confirmation, the database generates a 15-digit Temporary Reference Number (TRN) valid precisely for 15 days.

Phase 2: Comprehensive Application Data Submission (Part B)

Log back into the central portal using your validated TRN to unlock Form GST REG-01, Part B. You must provide clear documentation across these primary structural parameters:

- Constitution of Business: Incorporate official partnership deeds, MCA-issued certificates of incorporation, or formal LLPIN documentation.

- Principal Place of Business Proof: Submit non-blurry copies of electricity bills or municipal tax receipts coupled with structured, legally binding lease agreements or explicit NOCs on stamp paper for rented sites.

- Authorized Signatories: Map individual identity proofs, structural authorizations, and active primary mobile linkages.

Phase 4: Jurisdictional Assessment & Form GST REG-06 Issuance

Following successful ARN generation, the jurisdictional tax officer reviews the record. If the officer identifies defects or missing information, they issue a digital notice in Form GST REG-03 within 3 to 7 working days. The applicant has exactly 7 working days to submit a precise clarification via Form GST REG-04. If the documentation meets all legal benchmarks, the official registration certificate is issued digitally in Form GST REG-06, displaying your unique 15-digit Goods and Services Tax Identification Number (GSTIN).

3. Critical Post-Approval Enforcement Callouts

Securing your active GSTIN does not conclude your mandatory statutory onboarding responsibilities. Many new business owners expose themselves to sudden regulatory penalties due to omissions in post-registration timelines.

Under current operational advisories, all newly registered commercial entities must link a verified corporate bank account to the official GST portal within 30 days from GSTIN approval, or prior to the chronological filing date of their first GSTR-1/Invoice Furnishing Facility (IFF) return—whichever occurs earlier. Failure to complete this bank registration causes automated suspension of your GSTIN, blocking all sales processing and restricting your buyers from accessing Input Tax Credit (ITC).

4. Secure Premium Corporate Structuring via Validraft

Navigating complex jurisdictional tax laws, managing automated risk scores, and executing error-free corporate document submissions requires seasoned legal insight. Flawed data inputs risk permanent processing bans or long delays that stall commercial launches.

The elite team of corporate lawyers, chartered accountants, and company secretaries at Validraft handles end-to-end tax structuring, biometric coordination, and cross-state regulatory documentation with absolute legal precision. We insulate your enterprise from non-compliance risks right from day one.