West Bengal E-Way Bill Threshold Revised:

₹50,000 Limit Effective 1 June 2026

West Bengal E-Way Bill Threshold Revised for intra-state goods movement has been halved — from ₹1,00,000 to ₹50,000 — under Notification No. 02/2026-C.T./GST dated 22 May 2026.

New Threshold

Consignment Value

Effective Date

2026

Job Work

Exemption Intact

WB GST Rules

Sub-rule (14)

- New threshold: ₹50,000. The West Bengal E-Way Bill threshold for intra-state movement of goods has been revised downward from ₹1,00,000 to ₹50,000 with effect from 1 June 2026.

- Notification authority: Issued under Rule 138(14) of the West Bengal GST Rules, 2017, superseding Notification No. 03/2023-C.T./GST dated 18 December 2023.

- Job work exemption continues. No E-Way Bill is required for intra-state movement of goods related to job work — irrespective of consignment value — as defined under Section 2(68) of the CGST Act, 2017.

- Trade Circular issued. A clarificatory Trade Circular was published on 25 May 2026; businesses with implementation difficulties may represent before the Commissioner.

- Action required before 1 June 2026. Update invoicing systems, logistics workflows, and e-way bill generation thresholds on the GST E-Way Bill portal before the cut-off date.

The West Bengal E-Way Bill Threshold Revised by the Government of West Bengal through Notification No. 02/2026-C.T./GST dated 22 May 2026. The WB GST E-Way Bill ₹50,000 rule replaces the earlier ₹1,00,000 threshold and comes into force on 1 June 2026. Businesses, transporters, and logistics operators within West Bengal must update their compliance systems before this deadline to avoid penalties under the GST law.

This blog covers the full scope of the amendment — what changed, what remains exempt, the regulatory background, compliance steps, and applicable penalties — based on the official Kolkata Gazette notification and the Trade Circular issued on 25 May 2026.

📌 Official Source: Notification No. 02/2026-C.T./GST, published in The Kolkata Gazette (Extraordinary), No. WB(Part-I)/2026/SAR-180, dated 22 May 2026. Signed by Khalid Aizaz Anwar, IAS, Commissioner of State Tax, West Bengal.

1 What the West Bengal E-Way Bill Threshold Amendment Says

The amendment is issued in exercise of powers conferred by sub-rule (14) of Rule 138 of the West Bengal Goods and Services Tax Rules, 2017. The Commissioner of State Tax, West Bengal — in consultation with the Principal Chief Commissioner of Central Goods and Services Tax & Central Excise, Kolkata Zone — has, in the public interest, revised the intra-state e-way bill threshold.

In accordance with the earlier Notification No. 02/2023-C.T./GST dated 10 November 2023, an E-Way Bill is now required to be generated in respect of movement of goods originating and terminating within West Bengal where the consignment value exceeds ₹50,000 — except for intra-state movement of goods related to job work as defined under Section 2(68) of the CGST Act/WB GST Act, 2017.

| Parameter | Earlier Position | Revised Position (w.e.f. 1 Jun 2026) |

|---|---|---|

| Threshold for intra-state EWB | ₹1,00,000 | ₹50,000 |

| Applicability | Intra-state movement in West Bengal | Intra-state movement in West Bengal |

| Job work exemption | Exempt | Exempt (unchanged) |

| Governing rule | Rule 138(14), WB GST Rules | Rule 138(14), WB GST Rules |

| Superseded notification | 03/2023-C.T./GST dt. 18.12.2023 | 02/2026-C.T./GST dt. 22.05.2026 |

| Effective date | — | 1 June 2026 |

2 Regulatory Background — How West Bengal E-Way Bill Rules Evolved

The West Bengal GST administration has progressively tightened e-way bill requirements for intra-state movements since the GST framework was established. Understanding the regulatory trajectory provides context for the current amendment.

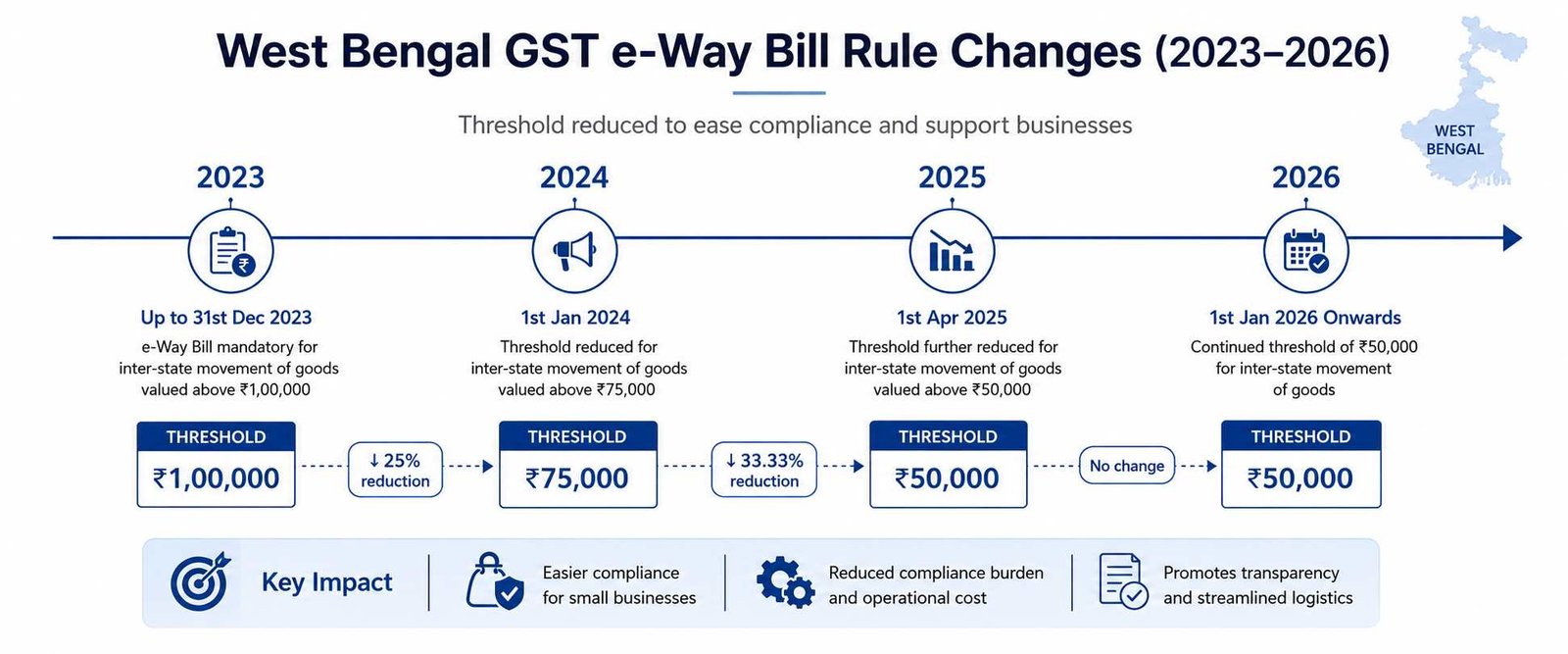

- 1 10 November 2023 Notification No. 02/2023-C.T./GST Framework notification aligning West Bengal’s intra-state e-way bill requirement with the national GST e-way bill structure under Rule 138.

- 2 18 December 2023 Notification No. 03/2023-C.T./GST Set the intra-state e-way bill threshold at ₹1,00,000 — effectively doubling the standard ₹50,000 limit applicable nationally, providing temporary administrative relief.

- 3 22 May 2026 Notification No. 02/2026-C.T./GST Supersedes the December 2023 notification. Restores the standard ₹50,000 threshold. Effective 1 June 2026. Published in Kolkata Gazette Extraordinary No. WB(Part-I)/2026/SAR-180.

- 4 25 May 2026 Clarificatory Trade Circular Trade Circular issued by the Directorate of Commercial Taxes, West Bengal, addressing implementation details and providing a representation mechanism for taxpayers facing practical difficulties.

3 WB GST E-Way Bill ₹50,000 — Who Is Affected

The revised WB GST E-Way Bill ₹50,000 threshold applies broadly to any person — supplier, recipient, or transporter — responsible for movement of goods within West Bengal where the consignment value crosses the revised limit. The following categories are directly impacted.

⚠️ Important: The consignment value for the purpose of e-way bill applicability includes the taxable value plus the applicable GST amount. A taxable value of ₹42,373 with 18% GST totals ₹50,000 and triggers the e-way bill requirement.

4 Job Work Exemption — Fully Preserved Under Revised Rules

The job work exemption under the West Bengal E-Way Bill threshold 2026 framework remains unchanged. No e-way bill is required for intra-state movement of goods relating to job work as defined under Section 2(68) of the CGST Act, 2017 / WB GST Act, 2017 — regardless of the consignment value involved.

✅ Movements Exempt from EWB

Goods sent by principal to registered job worker · Goods moved between job workers · Goods returned from job worker to principal — all exempt irrespective of value.

⚠️ Conditions for Exemption

The movement must qualify as “job work” under Section 2(68) of the CGST/WB GST Act. The principal must maintain a delivery challan as required under Rule 55 of the WB GST Rules, 2017.

✅ Job Work Definition (Section 2(68), CGST Act): “Job work means any treatment or process undertaken by a person on goods belonging to another registered person.” The exemption covers the principal’s goods — not the job worker’s own materials or finished goods dispatched for sale.

5 How to Generate an E-Way Bill for Intra-State Movement in West Bengal

The WB GST E-Way Bill ₹50,000 compliance process follows the standard national e-way bill framework. Generation is done on the e-way bill portal at ewaybillgst.gov.in. The steps below apply to intra-state movements within West Bengal effective 1 June 2026.

- Login to the E-Way Bill portal at ewaybillgst.gov.in using your GSTIN credentials.

- Click “Generate New” under the E-Way Bill menu. Select transaction type: Outward (if you are the supplier) or Inward (if you are the recipient generating EWB).

- Enter invoice details: Supply type, document type, document number, date, GSTIN of the counterparty, and place of delivery (West Bengal PIN code).

- Add item details: HSN code, product description, quantity, unit, taxable value, and applicable tax rates. Ensure the total consignment value — including GST — exceeds ₹50,000 to confirm EWB requirement.

- Enter transporter details: Vehicle number or transporter ID (if road transport). For other modes, provide the relevant transport document number.

- Generate EWB. The system creates a unique E-Way Bill Number (EBN). Share Part B details with the transporter if vehicle assignment is pending at generation time.

Portal: Generate, verify, and manage all West Bengal E-Way Bills at the national portal — ewaybillgst.gov.in. Sub-user creation and bulk upload (Excel/JSON) are available for high-volume dispatchers.

6 Penalties for Non-Compliance with WB GST E-Way Bill ₹50,000 Rule

Non-compliance with the WB GST E-Way Bill ₹50,000 requirement exposes the supplier, recipient, and transporter to significant financial and operational consequences under the GST law. The penalty provisions under the CGST Act and WB GST Act are identical in this regard.

⛔ Penalties Under Section 129 & 130, CGST/WB GST Act, 2017

- Detention of goods and vehicle: Goods found moving without a valid E-Way Bill above the prescribed threshold are liable to detention by a GST officer.

- Penalty — tax-paying goods: Payment of applicable tax plus penalty equal to 200% of the tax payable on the goods, OR ₹2,000, whichever is higher.

- Penalty — exempt goods: Penalty of 2% of the value of the goods or ₹25,000, whichever is lower.

- Confiscation (Section 130): Where the movement is found to be for evasion of tax, the goods and the conveyance are liable to confiscation.

- Transporter liability: The transporter is jointly and severally liable for penalty if they knowingly transport goods without a valid E-Way Bill.

7 Compliance Checklist for West Bengal Businesses — Before 1 June 2026

The West Bengal E-Way Bill threshold 2026 change requires operational adjustments across invoicing, dispatch, and logistics teams. Use the checklist below to ensure your business is compliant before the effective date.

📱 Portal Sub-User Access

If multiple staff generate EWBs, ensure all sub-users on ewaybillgst.gov.in are active and aware of the new ₹50,000 threshold. Update API integrations if your system uses bulk EWB generation via the GST portal API.

📝 Representation to Commissioner

The Trade Circular dated 25 May 2026 specifically permits taxpayers facing practical implementation difficulties to represent the matter before the Commissioner of State Tax, West Bengal. This is a formal relief channel available before penalties are imposed.

Need Help Updating Your GST Compliance Setup?

Validraft’s GST compliance team assists businesses in West Bengal and across India with e-way bill process review, GST return filings, and audit-ready documentation.

Get a Free Consultation → GST Services8 Implications for MSMEs and Small Traders in West Bengal

The revised West Bengal E-Way Bill threshold 2026 will have the most pronounced compliance impact on MSMEs, small traders, and distributors who operate primarily within the state. Consignments that previously moved without EWB formality — valued between ₹50,001 and ₹1,00,000 — now require documentation before dispatch.

For businesses engaged in intra-WB wholesale trade, consumer goods distribution, pharmaceutical supply chains, and auto parts distribution — where per-consignment values frequently fall in the ₹50,000–₹1,00,000 range — the volume of EWBs to be generated will increase materially. This is an administrative burden, not a tax cost, but non-compliance carries a penalty exposure that can significantly exceed the value of the consignment.

💡 Practical Note: If you currently use the GST portal’s bulk upload tool or an API-integrated ERP for EWB generation, update the threshold configuration parameter to ₹50,000 for West Bengal transactions. Most Tally, Busy, and SAP B1 implementations allow this to be changed under State-wise E-Way Bill Settings.

9 Conclusion — Act Before 1 June 2026

The West Bengal E-Way Bill threshold 2026 amendment is a firm regulatory tightening — not a procedural formality. From 1 June 2026, every intra-state movement of goods within West Bengal where the consignment value exceeds ₹50,000 must be accompanied by a valid e-way bill generated on the national GST portal. The WB GST E-Way Bill ₹50,000 limit now aligns West Bengal with the standard threshold applicable under the central GST framework.

Businesses that adjust their invoicing triggers, logistics SOPs, and transporter communications before the deadline will face no disruption. Those that do not risk detention of goods, vehicle seizure, and penalties of up to 200% of the applicable tax — consequences that far outweigh the effort of a one-time system update.

The job work exemption provides a carve-out for manufacturing supply chains dependent on third-party processing. For all other intra-state movements, the West Bengal E-Way Bill threshold 2026 leaves no room for interpretation: ₹50,000 is the new compliance line. Verify the current notification and any subsequent clarifications directly on the Directorate of Commercial Taxes, West Bengal portal before filing.

10 Frequently Asked Questions — WB GST E-Way Bill ₹50,000

📎 Authoritative Sources

- → Directorate of Commercial Taxes, West Bengal — wbcomtax.gov.in — Notification No. 02/2026-C.T./GST, dated 22.05.2026

- → GST E-Way Bill Portal — ewaybillgst.gov.in — E-Way Bill generation, verification, and cancellation

- → GSTN — gst.gov.in — Rule 138, CGST Rules, 2017 and Section 2(68), CGST Act, 2017