GST Registration for E-Commerce Sellers:

Rules, Threshold & Mistakes to Avoid

A verified, compliance-first guide for Amazon, Flipkart, Meesho sellers and independent online store owners — updated to reflect all changes effective April 2026.

TCS Rate

on Net Sales

To Register After

Becoming Liable

Minimum Penalty

Non-Registration

Govt. Registration

Fees (Free)

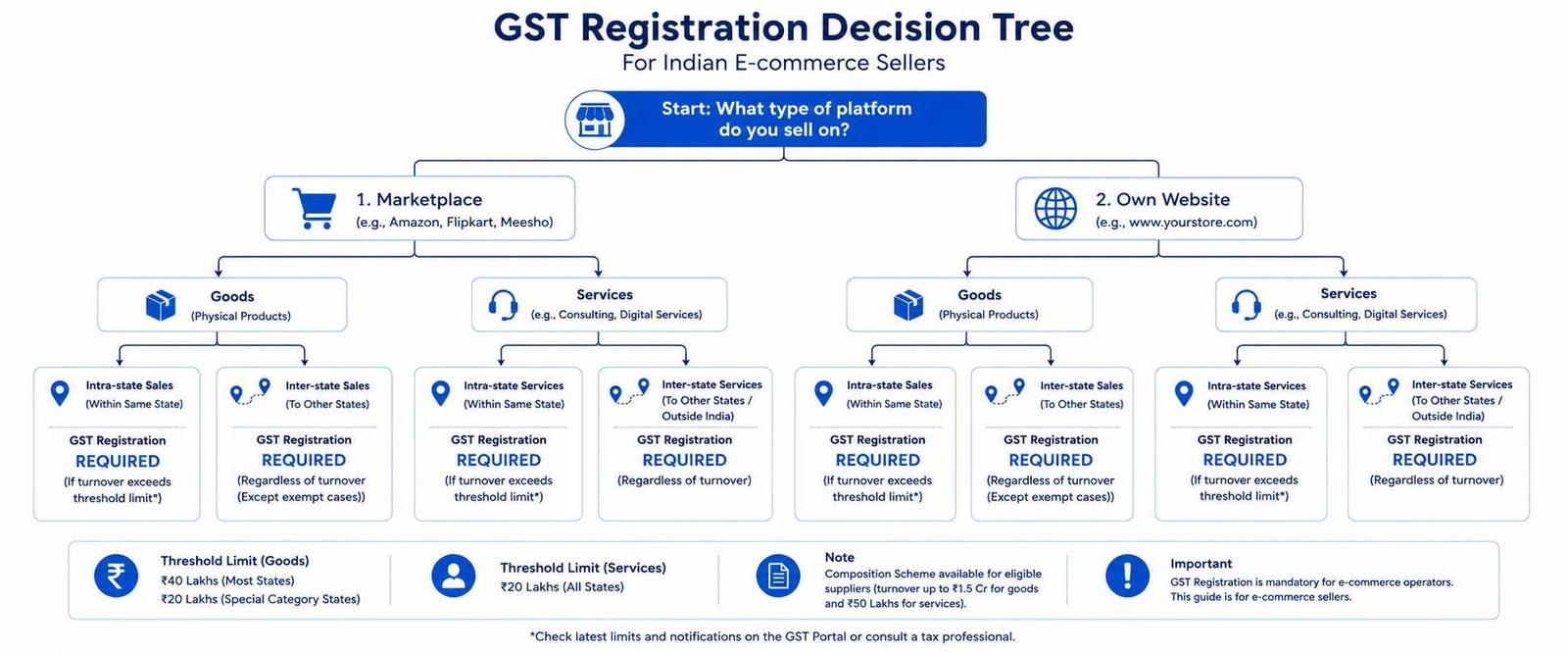

- Mandatory registration regardless of turnover: Under Section 24(ix) of the CGST Act, sellers supplying goods through e-commerce operators (ECOs) must register for GST — the normal ₹40 lakh / ₹20 lakh threshold does not protect them. Register at gst.gov.in.

- October 2023 exemption exists — but is narrow: Via Notification No. 34/2023-CT (effective 1 October 2023), small goods sellers operating only within one state/UT, with no inter-state sales, who hold a valid PAN and stay within the applicable threshold, are exempt from mandatory registration under Section 24(ix). Three conditions must all be satisfied simultaneously.

- Service sellers have a separate rule: Service providers supplying through ECOs with aggregate turnover below ₹20 lakh (₹10 lakh in special category states) are exempt — unless their services fall under Section 9(5) of the CGST Act.

- E-commerce operators deduct 1% TCS: Platforms like Amazon and Flipkart deduct Tax Collected at Source (TCS) at 1% (0.5% CGST + 0.5% SGST/UTGST for intra-state; 1% IGST for inter-state) before paying sellers. Sellers can claim this as a credit when filing returns.

- Penalty for non-registration: Under Section 122 of the CGST Act, the penalty is ₹10,000 or 10% of the tax due — whichever is higher. In cases of deliberate evasion, the penalty equals 100% of tax evaded (minimum ₹10,000).

GST registration for e-commerce sellers in India operates under a fundamentally different set of rules from those that apply to regular brick-and-mortar businesses. If you’re selling on Amazon, Flipkart, Meesho, or any other online marketplace — or running your own e-commerce website — the standard turnover threshold exemptions that protect most small businesses do not automatically apply to you. This guide provides a fully verified breakdown of the rules governing GST for online sellers, including the critical October 2023 amendment, the TCS mechanism, multi-state registration requirements, and the most common compliance mistakes that result in penalties and blocked listings.

1 Why E-Commerce Sellers Face Different GST Rules

The GST framework for e-commerce sellers is governed by two distinct provisions of the CGST Act, 2017: Section 22 (which sets the general turnover-based registration threshold) and Section 24 (which mandates registration for specific categories regardless of turnover). For most businesses, Section 22 applies — they must register only once their aggregate annual turnover crosses ₹40 lakh for goods or ₹20 lakh for services in regular states.

E-commerce sellers, however, fall under Section 24(ix), which mandates compulsory registration for “persons supplying goods or services through an electronic commerce operator who is required to collect tax at source under Section 52.” Because major platforms — Amazon, Flipkart, Meesho, Myntra, Snapdeal, and others — are required to collect TCS under Section 52, sellers on these platforms are brought into the compulsory registration net irrespective of their turnover.

Important distinction: If you sell goods exclusively through your own website without using a third-party marketplace that collects TCS, you are treated as a regular supplier under Section 22. GST registration is mandatory only once your turnover crosses the applicable threshold.

2 GST Registration Threshold for E-Commerce Sellers (April 2026)

The threshold rules for GST for online sellers differ based on whether you sell goods or services, whether you sell on a marketplace or through your own platform, and the state from which you operate. The table below summarises the applicable thresholds as verified against the CGST Act provisions effective April 2026.

| Seller Type | Normal States | Special Category States | Registration Trigger |

|---|---|---|---|

| Goods seller — marketplace (Amazon, Flipkart, etc.) | Mandatory regardless of turnover (Section 24(ix)) — unless Oct 2023 exemption applies | Same rule — Section 24(ix) applies | First taxable supply on platform |

| Goods seller — own website only | ₹40 lakh aggregate turnover | ₹20 lakh aggregate turnover | Crossing the annual threshold |

| Service seller — marketplace (not under Section 9(5)) | ₹20 lakh aggregate turnover | ₹10 lakh aggregate turnover | Crossing the annual threshold |

| Service seller — Section 9(5) services (cab aggregators, accommodation, housekeeping) | ECO pays tax — seller registration requirement shifts; ECO must register | Same | ECO registration mandatory; seller may be exempt if turnover below threshold |

| Inter-state supplier (any goods/services) | Mandatory — no threshold exemption | Mandatory — no threshold exemption | First inter-state taxable supply |

Special Category States (Lower Thresholds)

The following states have lower GST registration thresholds — ₹20 lakh for goods and ₹10 lakh for services: Arunachal Pradesh, Assam, Jammu & Kashmir, Himachal Pradesh, Manipur, Meghalaya, Mizoram, Nagaland, Sikkim, Tripura, and Uttarakhand. Sellers operating from or holding stock in these states must verify registration against the lower limits.

3 The October 2023 Exemption — What Changed and Who Qualifies

The CGST Amendment Act, 2023 (Act No. 30 of 2023), implemented via Notification No. 34/2023-CT dated 31 July 2023 and brought into force on 1 October 2023, introduced a limited exemption from the mandatory registration requirement under Section 24(ix). This is the most significant change to GST for online sellers in recent years and is frequently misunderstood.

What changed: Small goods sellers supplying exclusively through an ECO can now be exempt from mandatory registration under Section 24(ix) — but only if they satisfy all three prescribed conditions simultaneously.

Three Conditions for the Exemption

Intra-state supply only

The seller must not make any inter-state supply of goods. All sales must be within a single state or Union Territory. A single order shipped to a buyer in another state disqualifies the exemption.

Single state or UT of operation

The seller must operate in only one state or Union Territory. If you store inventory in multiple states — including through marketplace warehouses such as Amazon FBA fulfilment centres — you do not qualify.

Valid PAN + within applicable turnover threshold

The seller must possess a valid PAN issued under the Income Tax Act, 1961 and must have aggregate turnover within the applicable Section 22 threshold for their state (₹40 lakh for goods in normal states). Crossing the threshold removes the exemption and triggers mandatory registration under Section 22.

Who the exemption does NOT cover: Sellers making inter-state deliveries, sellers with stock in multiple states (including FBA warehouses), sellers of services under Section 9(5), and any seller whose turnover has crossed the applicable Section 22 threshold. For these sellers, GST registration for e-commerce sellers remains mandatory from the first rupee of turnover.

Composition Scheme After October 2023

Simultaneously with the above notification, Section 10 of the CGST Act was amended to permit small composite taxpayers to supply goods through ECOs on an intra-state basis. Composite taxpayers joining ECOs under this route are assigned enrolment numbers and remain subject to the composition scheme turnover limits (₹1.5 crore in normal states / ₹75 lakh in special category states). Critically, this applies only to goods sellers making intra-state supplies — composite scheme taxpayers still cannot make inter-state supplies through ECOs.

Note: E-commerce operators (the platforms themselves) who are liable to collect TCS under Section 52 cannot opt for the Composition Scheme. This restriction applies to the operator — not the individual seller.

4 Tax Collected at Source (TCS): How It Works for Sellers

Tax Collected at Source under Section 52 of the CGST Act is collected by e-commerce operators — not by the seller. Every marketplace that facilitates sales must collect TCS from the net taxable value of all supplies made through its platform and deposit it with the government. This is a direct mechanism that links your sales revenue to GST compliance.

TCS Rates (Current)

- Intra-state supply: 1% total (0.5% CGST + 0.5% SGST/UTGST)

- Inter-state supply: 1% IGST

- Applied on net taxable value — excluding GST, returns, and cancellations

- Deposited by the operator in GSTR-8 by the 10th of the following month

Seller’s Rights on TCS

- TCS deducted appears in your GSTR-2B as a credit

- Claim it in your electronic cash ledger when filing returns

- Adjust TCS credit against your GST output tax liability

- If TCS credit exceeds liability, claim a refund via the GST portal

Cash flow impact: The 1% TCS deduction reduces your receivables before you receive payment. Sellers with high-volume months can face working capital pressure. Reconcile your platform settlement statements with GSTR-2B every month to ensure the TCS credit is accurately reflected.

GSTR-8 Filed by the Operator — Not the Seller

Amazon, Flipkart, Meesho, and other ECOs file GSTR-8 monthly by the 10th of the following month, reporting all TCS collected. This data auto-populates in your GSTR-2B. As a seller, you must still independently file GSTR-1 and GSTR-3B — the operator’s GSTR-8 filing does not replace your return obligations.

5 GST Registration Process for E-Commerce Sellers — Step by Step

GST registration is processed entirely online at gst.gov.in at no government fee. You must apply within 30 days from the date you become liable for registration. Late application attracts penalties from the date of liability — not the date of application.

Visit gst.gov.in → Services → Registration → New Registration

Select “Taxpayer” as the type. Enter your legal name (matching PAN), state, email, and mobile number. An OTP will be sent to your mobile and email for verification. A Temporary Reference Number (TRN) is generated.

Complete Part B of REG-01 using the TRN

Log in with the TRN and complete all sections: business details, principal place of business, additional places of business, goods and services (HSN codes), bank account details, and authorised signatory information.

Upload documents (PDF/JPG, max 1 MB per file)

PAN, Aadhaar, proof of business address (electricity bill, rent agreement, or ownership document), bank statement or cancelled cheque, photograph of the proprietor/authorised signatory, and entity constitution documents as applicable.

Aadhaar authentication / biometric verification

As per CBIC Central Tax Instruction No. 03/2025-GST (April 2025), place-of-business verification is strictly enforced. Aadhaar-based e-authentication or biometric verification at a GST Suvidha Kendra may be required depending on your risk category. Complete this promptly — delay holds the application.

ARN generated → GSTIN issued

On successful submission, an Application Reference Number (ARN) is generated for tracking. As of November 2025, the GSTN’s automated AI-based system approves approximately 96% of applications within 3 working days. Bank account details must be furnished within 30 days of registration or before filing GSTR-1 to avoid suspension (GSTN advisory, 20 November 2025).

Documents Checklist for E-Commerce Seller Registration

📋 Common Documents (All Entities)

- PAN card of business/proprietor

- Aadhaar card of proprietor/directors/partners

- Proof of business address (latest utility bill or rent agreement)

- Cancelled cheque or bank account statement

- Passport-size photograph of authorised signatory

- Digital Signature Certificate (mandatory for companies and LLPs)

🛒 Additional for E-Commerce Sellers

- Marketplace seller agreement or vendor code proof

- Proof of warehouse/inventory address if different from principal place

- Partnership deed / MOA & AOA / LLP agreement (as applicable)

- Authorisation letter for authorised signatory

- Board resolution (for companies)

- HSN codes for all goods being sold

6 GST Return Filing Obligations for Online Sellers

Once registered, GST for online sellers requires monthly compliance. E-commerce sellers on marketplaces are classified as regular taxpayers and cannot use the Composition Scheme (which simplifies filing to quarterly statements). Most marketplace sales are inter-state, attracting IGST rather than CGST + SGST — ensure your invoices reflect the correct tax type.

| Return | What It Covers | Due Date | Applies To |

|---|---|---|---|

| GSTR-1 | Outward supplies (sales) — invoice-level details | 11th of following month (turnover > ₹5 crore); Quarterly under QRMP scheme for ≤ ₹5 crore | All registered sellers |

| GSTR-3B | Summary return — tax liability, ITC claimed, TCS credit adjusted | 20th of following month (monthly filers) | All registered sellers |

| GSTR-9 | Annual return reconciling all monthly filings | 31 December of following financial year | Turnover above ₹2 crore (below ₹2 crore exempt for FY 2023-24 per 53rd GST Council) |

| GSTR-8 | TCS collected from sellers — filed by the operator, not the seller | 10th of following month | E-commerce operators only |

2026 critical rule: As of December 2025, the GST portal permanently blocks filing of returns older than three years from their original due date. A nil return filed 3+ years late cannot be submitted. The portal enforced this cutoff from 1 December 2025. Do not let any return period remain unfiled — even nil returns must be filed on time.

E-Invoicing for E-Commerce Sellers

E-invoicing — generating invoices through the IRP (Invoice Registration Portal) with a unique IRN — is mandatory for registered businesses with aggregate annual turnover exceeding ₹5 crore. For sellers above ₹10 crore, invoices must be reported to the IRP within 30 days of the invoice date to generate a valid IRN. Failure to comply blocks Input Tax Credit for your buyers and can result in supply disruptions.

7 Multi-State Registration: A Requirement Many Sellers Miss

One GSTIN covers one state or Union Territory. If your business has a taxable presence in more than one state, you need separate GST registration in each state. For e-commerce sellers, this requirement is triggered more often than it appears — and missing it is a compliance risk.

Amazon FBA / Flipkart warehouse sellers — this applies to you: If Amazon, Flipkart, or any other marketplace stores your inventory in a fulfilment centre located in another state, that warehouse constitutes your “additional place of business” in that state under GST law. You must obtain a separate GSTIN for that state and report the warehouse as an additional place of business.

What Triggers Multi-State Registration

Each GSTIN requires separate return filing (GSTR-1, GSTR-3B, GSTR-9), separate Input Tax Credit tracking, and separate bank account linkage. Plan your warehouse footprint carefully — the tax compliance cost of multi-state registrations is proportional to the number of states you operate in.

Need GST Registration for Your E-Commerce Business?

Validraft’s compliance team handles GST registration, multi-state GSTIN applications, and ongoing return filing for online sellers across India.

Get a Free Consultation → View GST Services8 7 GST Mistakes E-Commerce Sellers Must Avoid

❌ Mistake 1: Assuming the ₹40 Lakh Threshold Applies to Marketplace Sales

The most common mistake among new sellers. Section 24(ix) overrides the general Section 22 threshold for marketplace sellers. Unless you satisfy all three conditions of the October 2023 exemption, you are required to register before making your first taxable supply on the platform.

✅ Fix: Register before listing on any ECO platform. Apply at gst.gov.in with a minimum 7–10 day buffer before your first sale.

❌ Mistake 2: Not Registering in States Where FBA Warehouses Hold Your Stock

Sellers enrolled in Amazon FBA or similar marketplace fulfilment programmes often have inventory warehoused across multiple states without realising it constitutes a taxable presence. Using a Mumbai-registered GSTIN for stock stored in a Bengaluru fulfilment centre is non-compliant.

✅ Fix: Check your marketplace seller dashboard for the states where your inventory is stored. Obtain a separate GSTIN in each such state and declare the warehouse as an additional place of business.

❌ Mistake 3: Using CGST + SGST for Inter-State Sales

Most e-commerce sales ship across state borders. These are inter-state supplies and attract IGST — not CGST and SGST. Raising invoices with the wrong tax heads results in incorrect input tax credit for buyers and potential demands from the department.

✅ Fix: Determine the buyer’s delivery state before generating each invoice. For intra-state: split into CGST + SGST. For inter-state: charge IGST at the applicable rate.

❌ Mistake 4: Not Reconciling GSTR-2B with Platform TCS Data

E-commerce operators file GSTR-8 by the 10th of the following month. This auto-populates in your GSTR-2B as TCS credit. If the platform reports a different net taxable value than your own records (due to returns, cancellations, or settlement errors), the mismatch leads to ITC errors in your GSTR-3B.

✅ Fix: Download your platform settlement report every month. Cross-check net taxable sales with GSTR-2B entries. Report discrepancies to the marketplace before filing GSTR-3B.

❌ Mistake 5: Missing Credit Note Timelines for Customer Returns

When a customer returns a product, you must issue a credit note to reverse the GST charged. A credit note must be issued within the same financial year as the original supply. Missing this window means you cannot reverse the GST already paid, resulting in an irrecoverable tax cost.

✅ Fix: Track return orders monthly. Issue credit notes within the same financial year. Platforms like Amazon auto-process some adjustments — verify these against your GSTR-2B and your own credit note register.

❌ Mistake 6: Applying the Composition Scheme as a Marketplace Seller

Prior to October 2023, e-commerce marketplace sellers were entirely excluded from the Composition Scheme. After October 2023, only small intrastate goods sellers meeting all three exemption conditions may use it. Any seller making inter-state sales through an ECO cannot use the Composition Scheme — attempting to do so results in returns rejection and demands.

✅ Fix: If you make inter-state sales on any marketplace, file as a regular taxpayer — GSTR-1 and GSTR-3B monthly or quarterly as applicable. Confirm your scheme eligibility with a GST practitioner before opting.

❌ Mistake 7: Delaying Registration After Becoming Liable

Registration must be applied for within 30 days from the date you become liable. Delayed registration attracts backdated tax liability from the date of liability onset — not the date of actual registration. Additionally, under Section 122, the penalty is ₹10,000 or 10% of tax due (whichever is higher), plus 18% interest on unpaid tax.

✅ Fix: Apply for GST registration before your first marketplace listing or before making your first inter-state supply. Do not wait for a full sales cycle.

9 Penalties for GST Non-Compliance — E-Commerce Sellers

The CGST Act prescribes specific penalties for failing to register when mandatory, for incorrect invoicing, and for TCS-related non-compliance. The penalty structure under Section 122 is not discretionary — once an offence is established, the penalty applies as a statutory minimum.

| Offence | Penalty | Legal Provision |

|---|---|---|

| Failure to register when mandatory | ₹10,000 or 10% of tax due — whichever is higher | Section 122(1), CGST Act |

| Deliberate evasion / fraud in non-registration | 100% of tax evaded (minimum ₹10,000) + 18% interest | Section 122(2)(b), CGST Act |

| Supplying without invoice or incorrect invoice | ₹10,000 or equivalent to tax involved — whichever is higher | Section 122(1)(i), CGST Act |

| Wrong ITC claim (fake invoices) | 100% of ITC wrongly availed (minimum ₹10,000) | Section 122(1)(vii), CGST Act |

| Late filing of GSTR-1 / GSTR-3B | ₹50/day (₹20/day for nil returns) — capped at ₹5,000 per return | Section 47, CGST Act |

| General contravention (no specific provision) | Up to ₹25,000 | Section 125, CGST Act |

Note on Section 122(1B): The penalty provision for e-commerce operators allowing unregistered sellers on their platforms was amended retrospectively from 1 October 2023 via the Finance (No. 2) Act, 2024. This provision applies to operators required to collect TCS under Section 52 — the platform itself bears liability if it allows non-compliant sellers to list goods. This gives platforms a commercial incentive to enforce GSTIN verification on all sellers.

10 Conclusion: GST Registration for E-Commerce Sellers Is Non-Negotiable

GST registration for e-commerce sellers is not a formality to complete after your business gains traction — it is a precondition for operating legally on any marketplace in India. The rules under Section 24(ix) of the CGST Act are designed to ensure that the TCS mechanism functions effectively, and non-registration disrupts the entire tax chain. Whether you sell on Amazon, Flipkart, Meesho, or any other ECO, your compliance obligations begin before your first sale.

The October 2023 amendment has provided some relief to genuinely small, intrastate goods sellers — but the three-condition eligibility test is strict. Inter-state sellers, multi-warehouse operators, and service providers under Section 9(5) remain outside the exemption scope. Understanding precisely where you stand in the GST for online sellers framework determines your registration timeline, your return filing frequency, and your exposure to penalties.

At Validraft, our compliance team assists e-commerce sellers with GST registration for e-commerce sellers across all entity types — proprietorships, partnerships, LLPs, and private limited companies — including multi-state GSTIN applications, FBA warehouse compliance, GSTR-1 and GSTR-3B filing, and TCS credit reconciliation. Contact us via validraft.in/contact to get your registration done accurately before it becomes a liability.

Register Your GST for E-Commerce — Accurately and On Time

Avoid penalties, listing blocks, and backdated tax demands with Validraft’s end-to-end GST compliance service for online sellers.

Start Registration → GST Services11 Frequently Asked Questions — GST for Online Sellers

📎 Authoritative Sources

- → GST Portal — gst.gov.in — Official GST registration portal (Section REG-01 / Form GST REG-01)

- → CBIC GST — cbic-gst.gov.in — Central Board of Indirect Taxes and Customs; CGST Act 2017, Section 24(ix) and Section 52

- → CBIC Tax Information Portal — CGST Act Section 24 (compulsory registration), Section 122 (penalties), Notification No. 34/2023-CT dated 31 July 2023, effective 1 October 2023

- → PIB — 53rd GST Council Meeting Recommendations — Annual return exemption for turnover up to ₹2 crore, Section 122(1B) clarification

- → GST Portal Advisories — GSTN Advisory on bank account details (20 November 2025); CBIC Instruction No. 03/2025-GST (17 April 2025)