GST Registration for Freelancers & Independent Consultants:

Do You Actually Need It?

A compliance guide for India’s gig economy — thresholds, mandatory triggers, export rules, and when voluntary registration makes strategic sense.

Mandatory GST

Threshold (Services)

GST Rate on Most

Freelance Services

GST on Export

of Services

Late Filing Penalty

per Day (capped ₹2,000)

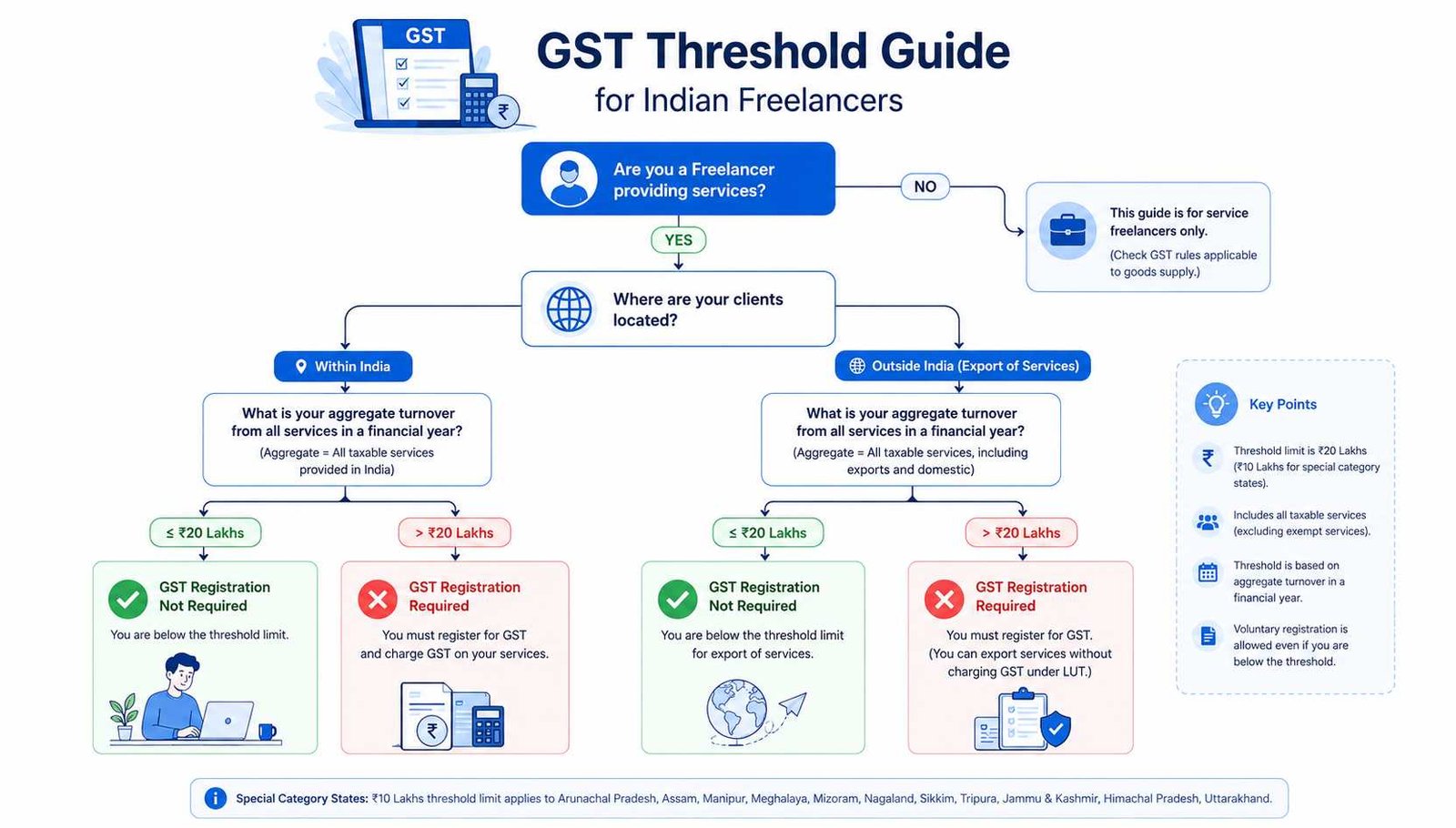

- Mandatory threshold is ₹20 lakh aggregate turnover for service providers in normal-category states, and ₹10 lakh in special-category states (NE states + Uttarakhand) — under Section 22 of the CGST Act, 2017.

- Interstate service exemption applies — freelancers below the ₹20 lakh threshold are not required to register even for interstate client work, per Notification No. 10/2017-IGST (Rate).

- Export of services is zero-rated — foreign-currency freelance income attracts 0% GST; file a Letter of Undertaking (LUT) in Form RFD-11 on gst.gov.in before each financial year.

- 18% GST applies to most professional services — SAC code 9983 covers IT consulting, design, content, and management consulting.

- Voluntary registration is strategically valuable for freelancers serving corporate B2B clients or planning to scale past the threshold within 6–12 months.

GST registration for freelancers is one of the most misunderstood compliance requirements in India. The gig economy has grown faster than tax literacy, leaving thousands of independent professionals unsure whether they need to register, when to do it voluntarily, and what happens if they don’t. This guide cuts through the confusion. It covers every scenario relevant to GST for consultants in India — from the basic ₹20 lakh threshold to export rules, SAC codes, return obligations, and the exact registration process on the government portal.

Whether you’re a graphic designer billing ₹8 lakh a year from Indian startups, a management consultant earning ₹35 lakh from corporate clients, or a software developer with overseas clients paying in USD, your compliance obligations are materially different. Understanding that difference is what separates a clean audit trail from a penalty notice.

1 The ₹20 Lakh Rule: When GST Registration for Freelancers Becomes Mandatory

Under Section 22 of the CGST Act, 2017, any person supplying taxable services whose aggregate turnover in a financial year exceeds ₹20 lakh is required to obtain GST registration. This threshold is not based on profit — it is based on the total value of all services supplied, including both taxable and exempt supplies, calculated from 1 April to 31 March each year.

| State Category | Mandatory GST Threshold | States Included |

|---|---|---|

| Normal Category States | ₹20 lakh per financial year | Maharashtra, Karnataka, Delhi, Gujarat, Tamil Nadu & most others |

| Special Category States | ₹10 lakh per financial year | Manipur, Mizoram, Nagaland, Meghalaya, Tripura, Arunachal Pradesh, Sikkim, Uttarakhand |

The aggregate turnover calculation includes all income streams tied to the same PAN — freelance work, consulting retainers, commission income, and rental income, if any. It does not deduct expenses or GST collected. A freelancer earning ₹18 lakh from content writing and ₹4 lakh from training workshops crosses the threshold even if each income stream individually falls below ₹20 lakh.

⚠ Common Misconception: Many freelancers assume the ₹20 lakh threshold applies per client or per service category. It does not. Aggregate turnover means the combined total from all services, across all clients, in the financial year — regardless of how income is categorised.

2 When Mandatory Registration Applies Below the ₹20 Lakh Threshold

Several categories of freelancers and consultants must register for GST even if annual turnover is below ₹20 lakh. These mandatory registration triggers under Section 24 of the CGST Act operate independently of the threshold.

Notably, pure inter-state service suppliers below the ₹20 lakh threshold are exempt from compulsory registration under Notification No. 10/2017-IGST (Rate). A Delhi-based freelance consultant billing clients in Mumbai or Bengaluru does not need GST registration solely because of those interstate transactions — provided aggregate turnover stays under ₹20 lakh and no other mandatory trigger applies.

3 GST Rates and SAC Codes for Freelancers and Consultants

GST for consultants in India applies at 18% for nearly all professional and technical services. This rate breaks down as 9% CGST + 9% SGST for intra-state supplies, or 18% IGST for inter-state supplies. The applicable Service Accounting Codes (SAC) under the GST tariff determine the rate and how services are reported in returns.

| Service Type | SAC Code | GST Rate |

|---|---|---|

| IT consulting, software development | 998313 / 998314 | 18% |

| Management consulting, business advisory | 998311 | 18% |

| Content writing, copywriting, editorial | 998392 | 18% |

| Graphic design, digital art, UI/UX | 998392 / 998741 | 18% |

| Digital marketing, SEO, social media | 998399 | 18% |

| Legal advisory (to business entities) | 998212 | 18% (RCM may apply) |

| Export of services (foreign clients) | All applicable | 0% (Zero-rated) |

The correct SAC code must be mentioned on every tax invoice. Misclassifying services or applying the wrong rate can result in discrepancies during GST audits and ITC mismatches for clients. If you’re a multi-disciplinary consultant — say, combining strategy and digital delivery — use the SAC code that corresponds to the primary nature of the service billed on each invoice.

4 The Strategic Case for Voluntary GST Registration

Voluntary GST registration is available to any freelancer or independent consultant regardless of turnover. Once registered, all compliance obligations — return filing, invoice requirements, payment timelines — apply in full. The decision to register voluntarily should be driven by specific business circumstances, not by general advice to “get a GSTIN.”

✅ Strong Reasons to Register Voluntarily

- Corporate and MNC clients require a GST invoice to claim Input Tax Credit (ITC)

- Approaching the ₹20 lakh threshold within 6–12 months — register proactively rather than reactively under penalty

- Serving international clients and want to export under LUT to claim ITC refunds

- Claiming ITC on business expenses: software subscriptions, internet, co-working space, professional equipment

❌ Weak Reasons to Register Voluntarily

- Turnover is below ₹10 lakh with no corporate clients and no plans to scale

- All clients are individuals who cannot claim ITC — a GSTIN adds no business value

- You lack bandwidth for monthly/quarterly return filing — non-compliance after registration attracts penalties

- You believe registration itself reduces tax liability — it does not; it only changes how tax is collected and passed on

Important: Once voluntarily registered, you cannot selectively file returns. GSTR-1 and GSTR-3B are mandatory every period — even if you have zero taxable supplies that month. Missing a nil return attracts a late fee of ₹20 per day (capped at ₹500). Verify all requirements at gst.gov.in.

Not Sure If You Need GST Registration?

Validraft’s compliance team assesses your turnover profile, client base, and export income to give you a clear answer — and handles the entire registration if needed.

Get a Free Consultation → GST Services5 GST for Freelancers with Foreign Clients: The Export-of-Services Framework

Export of services is zero-rated under Section 16 of the IGST Act, 2017 — meaning no GST is charged to the foreign client, and the supplier can recover Input Tax Credit on domestic business expenses. This is one of the most significant financial benefits available to freelancers working with international clients.

For a supply to qualify as “export of services” under Section 2(6) of the IGST Act, five conditions must be met simultaneously: the supplier must be located in India; the recipient must be outside India; the place of supply must be outside India; payment must be received in convertible foreign currency or Indian rupees when permitted by RBI; and the supplier and recipient must not be merely establishments of the same person.

Register for GST (Voluntary, Recommended)

Even if turnover is below ₹20 lakh, registration is advisable for export-oriented freelancers who want to claim ITC refunds on domestic expenses.

File a Letter of Undertaking (LUT) — Form GST RFD-11

File the LUT on gst.gov.in before the start of each financial year. This allows you to export services without paying IGST. LUT is valid for one financial year and must be renewed annually.

Issue a Zero-Rated Export Invoice

Invoice must include: “Supply meant for export under bond/LUT without payment of IGST.” Report in GSTR-1 under the Exports section with correct port code.

Maintain FIRC / Bank Realisation Certificate (BRC)

Foreign Inward Remittance Certificates (FIRCs) issued by your bank or payment gateway are required for ITC refund claims. Collect FIRCs for every foreign payment received. The e-BRC process applies from November 2023.

Claim ITC Refund — Form GST RFD-01

File Form GST RFD-01 within 2 years of the relevant date to claim refund of unutilised ITC on domestic inputs used for export services. Refer to Rule 89 of CGST Rules for documentation.

6 GST Returns Freelancers Must File After Registration

Once registered — whether mandatory or voluntary — a freelancer must file returns consistently. As of July 2025, GSTR-3B introduced hard-locking of auto-populated tax liability fields. All adjustments must be completed in GSTR-1 or GSTR-1A before submitting GSTR-3B. No manual amendments to tax liability are permitted after GSTR-3B is filed. This makes invoice accuracy in GSTR-1 non-negotiable.

Freelancers whose annual turnover is below ₹5 crore can opt for the Quarterly Return Monthly Payment (QRMP) scheme — filing GSTR-1 and GSTR-3B quarterly while making monthly tax payments via a fixed payment challan. This reduces the annual return-filing burden from 24 filings to 8. The Composition Scheme under Section 10(2A) is also available for service providers with turnover up to ₹50 lakh, at a flat 6% rate — but bars ITC claims and inter-state supply.

7 Penalties for Non-Compliance: What GST for Consultants in India Costs If Ignored

Non-registration after crossing the ₹20 lakh threshold — or failure to file returns after registration — carries specific penalties under the CGST Act. These penalties are not discretionary; they are calculated and enforced systematically through the GST portal.

| Violation | Penalty / Late Fee | Cap |

|---|---|---|

| Late GSTR-1 or GSTR-3B filing | ₹50 per day (₹25 CGST + ₹25 SGST) | ₹2,000 per return |

| Nil return filed late | ₹20 per day (₹10 CGST + ₹10 SGST) | ₹500 per return |

| Non-registration (mandatory) | 10% of tax due or ₹10,000 — whichever is higher | No cap for intentional evasion |

| Interest on unpaid tax | 18% per annum on outstanding tax amount | Calculated daily |

| Failure to file returns older than 3 years | Permanent non-acceptance on GST portal after December 2025 | Irrecoverable compliance gap |

⚠ December 2025 Deadline (Passed): Per the October 2025 GST advisory, returns older than three years from their original due date are no longer accepted on the GST portal as of December 1, 2025. Freelancers with unfiled returns from FY 2021–22 or earlier face a permanent compliance gap. Consult gst.gov.in for current rectification procedures.

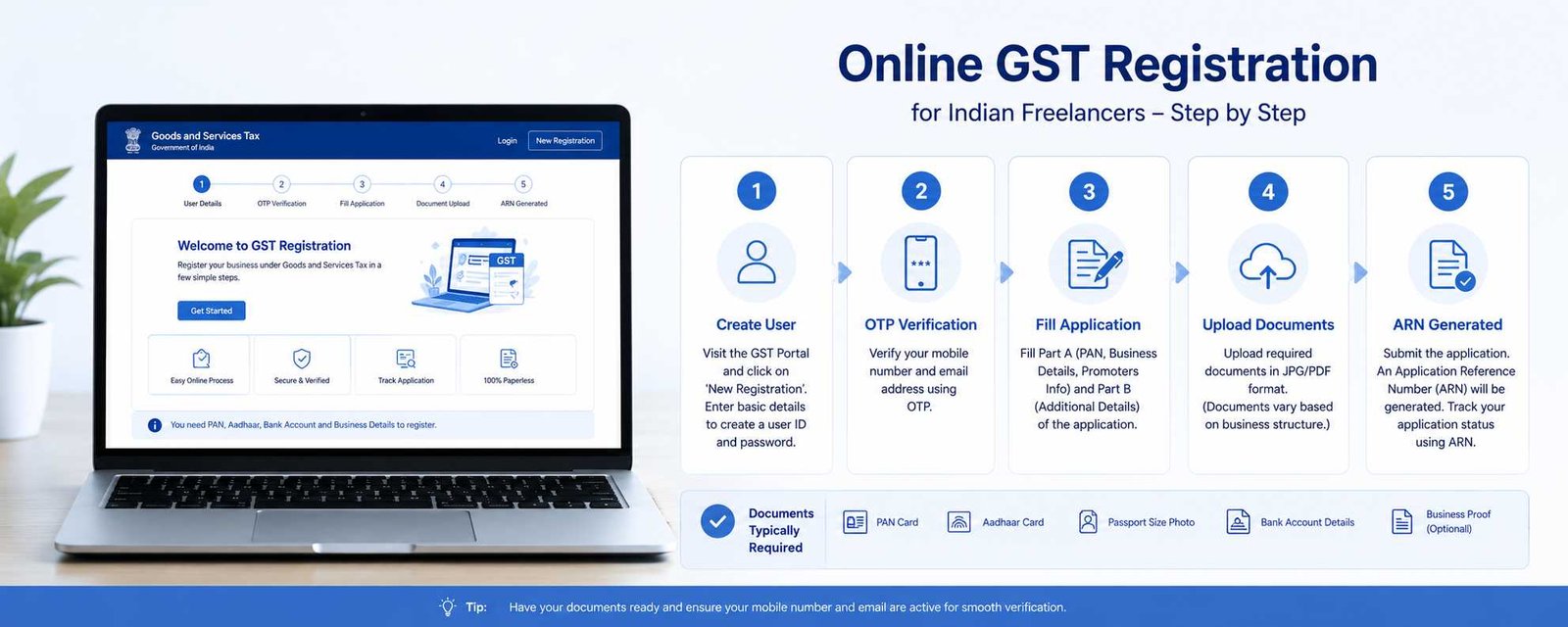

8 How to Register for GST as a Freelancer: Step-by-Step Process on gst.gov.in

GST registration is a fully online process completed on the GST portal. There are no government fees for registration. The process typically completes within 7–10 working days from application, assuming documentation is in order and no clarification is sought by the GST officer.

Part A — Generate TRN

Visit gst.gov.in → Services → Registration → New Registration. Enter PAN, mobile number, and email. Verify OTPs. A Temporary Reference Number (TRN) is generated and valid for 15 days.

Part B — Complete Application

Log in using TRN. Enter business details: legal name (as on PAN), principal place of business, nature of services, and SAC codes. Select “Freelancer” or “Sole Proprietor” as business type.

Upload Documents

PAN card, Aadhaar (for authentication), a cancelled cheque or bank statement (for bank details), and a photograph. For address proof: rental agreement, electricity bill, or NOC from property owner.

Aadhaar Authentication or Physical Verification

Opt for Aadhaar-based e-authentication (faster) or physical verification by a GST officer. Aadhaar authentication typically reduces processing time by 2–3 days.

Receive GSTIN and Registration Certificate

Once the application is approved, a 15-digit GSTIN and Form GST REG-06 (registration certificate) are issued to your registered email. Download the certificate from the portal. No physical certificate is issued.

9 Conclusion: Making the Right GST Decision for Your Freelance or Consulting Practice

GST registration for freelancers is not a one-size-fits-all requirement. If your aggregate turnover is below ₹20 lakh, you provide services only within India, and your clients are individuals who derive no benefit from a GSTIN, there is no legal compulsion and no tactical advantage to registering. The compliance burden would outweigh any upside.

The calculus changes the moment you cross the threshold, work with corporate clients who need to claim ITC, earn in foreign currency, or anticipate growth that will take you past ₹20 lakh within the year. In those scenarios, GST for consultants in India is not a burden — it’s a credentialing tool that opens access to larger, more structured client relationships. Voluntary registration done correctly, with an LUT filed for export clients and a quarterly return schedule in place, is a net positive for any scaling freelancer.

The critical variable is preparation. GST registration for freelancers who are reactive — registering after crossing the threshold, catching up on missed returns, or applying for an LUT after already invoicing foreign clients without one — is significantly more costly in time, fees, and penalty risk than proactive, structured compliance. Validraft’s team works with independent professionals to assess their current position, determine the right registration strategy, and manage end-to-end compliance so billing stays uninterrupted.

Get Your GST Registration and Compliance Right — First Time

Validraft handles GST registration, LUT filing, return management, and ITC refund claims for freelancers and independent consultants across India.

Talk to a GST Expert → View GST ServicesFrequently Asked Questions — GST Registration for Freelancers India

No — provided your aggregate turnover (all income sources, same PAN) stays below ₹20 lakh in the financial year and you’re not in a special category state. You are not required to register for GST registration for freelancers at this level, even if you supply to clients in different states. However, voluntary registration is available and may be worth considering if corporate clients require a GST invoice. Verify current thresholds at cbic-gst.gov.in.

If your services qualify as “export of services” under Section 2(6) of the IGST Act — foreign recipient, foreign currency payment, place of supply outside India — then the supply is zero-rated. No GST is charged to your client. If you’re registered under GST for consultants in India and have filed an LUT, you can also claim refund of accumulated ITC on your business expenses through Form GST RFD-01. Without registration, you forgo this benefit but also have no filing obligation if turnover is below ₹20 lakh.

Use the SAC code that best describes the primary nature of services on each invoice. Management and business consulting: 998311. IT consulting and software services: 998313 or 998314. Content writing and editorial: 998392. Digital marketing: 998399. If you provide mixed services, apply the SAC of the dominant service component on that invoice. The correct SAC code is required on all GST tax invoices and reported in GSTR-1. Misclassification can cause ITC mismatches for your clients.

Yes. Service providers with aggregate turnover up to ₹50 lakh can opt for the Composition Scheme under Section 10(2A) of the CGST Act, which applies a flat 6% rate (3% CGST + 3% SGST). However, the scheme bars ITC claims, prohibits inter-state supply, and does not permit export of services under LUT. For most freelancers with corporate B2B clients or foreign clients, the standard GST registration route is more beneficial. Verify current Composition Scheme eligibility at gst.gov.in.

Under Section 122 of the CGST Act, failure to obtain mandatory GST registration attracts a penalty of 10% of the tax amount due, subject to a minimum of ₹10,000. For cases involving deliberate tax evasion, the penalty can be 100% of the tax due. Additionally, interest at 18% per annum applies to unpaid tax for the period of non-registration. A freelancer who crosses the ₹20 lakh threshold and delays registration by several months can accumulate significant liability. Apply for GST registration for freelancers proactively, before crossing the threshold.

Yes. A voluntarily registered taxpayer can apply for cancellation under Section 29(1) of the CGST Act if they no longer wish to be registered — provided their turnover has not crossed the mandatory threshold. The cancellation application is filed in Form GST REG-16 on the GST portal. All pending returns must be filed and dues cleared before cancellation is granted. A final return in Form GSTR-10 (within 3 months of cancellation) is also required.

📎 Authoritative Sources

- → CBIC — Central Goods and Services Tax Act, 2017 (Section 22, 24, 29, 122)

- → GST Portal — Registration, LUT filing, Return filing (gst.gov.in)

- → CBIC — Integrated Goods and Services Tax Act, 2017 (Section 2(6), 16)

- → Notification No. 10/2017-IGST (Rate) — Interstate service exemption for small providers