Sole Proprietorship vs Private Limited Company 2026:

Tax, Liability & Compliance Compared

A complete side-by-side comparison for first-time founders choosing the right business structure in India — with a decision framework and comparison table.

Govt Setup Cost

Sole Proprietorship

Min. Govt Fee

Pvt Ltd (MCA)

Corporate Tax

Pvt Ltd (Sec 115BAA)

Pvt Ltd Incorporation

Off-Peak Timeline

- Liability is the core difference: a sole proprietor has unlimited personal liability — your personal assets are at risk. A private limited company provides limited liability protection under Companies Act 2013.

- Tax treatment diverges sharply: sole proprietors are taxed at individual income tax slab rates (up to 30%), while a private limited company pays a flat 22% corporate tax (under Section 115BAA) — plus surcharge and cess, effective ~25.17%.

- Compliance burden is far higher for Pvt Ltd: expect 8–10 mandatory MCA filings per year, two statutory audits, and a minimum of four board meetings annually. Sole proprietors have minimal regulatory obligations.

- Funding and credibility favour Pvt Ltd: venture capital, angel investment, and bank credit are significantly easier to access as a private limited company. Equity cannot be issued in a sole proprietorship.

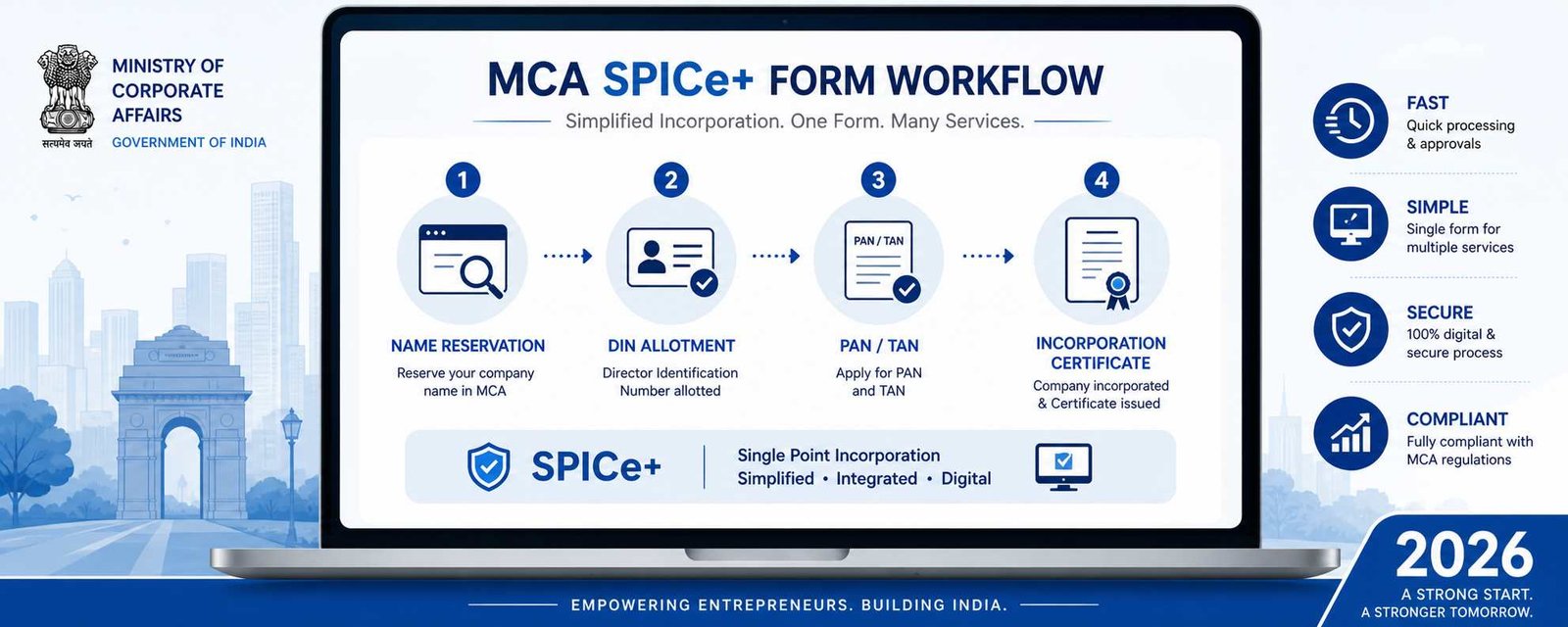

- Government incorporation fee for Pvt Ltd starts at ₹1,443 (for ₹1 lakh authorised capital) via SPICe+ — verify the latest fee schedule at mca.gov.in.

Choosing between a sole proprietorship vs private limited company is the first — and most consequential — structural decision every founder in India must make. The business structure you register today shapes your tax outgo, personal risk exposure, fundraising ability, and long-term compliance cost for years. This guide compares both structures across every dimension that matters for a first-time founder navigating the Indian business landscape in 2026.

Whether you’re a freelancer testing a service idea or a founder building for scale, understanding the business structure India framework — the legal basis, tax treatment, and real operational differences — is essential before you file a single form.

1 What Is a Sole Proprietorship in India?

A sole proprietorship is the simplest business form in India. There is no separate registration statute — the business and the owner are legally the same entity. You start trading under your own name or a trade name, and the law treats all profits, liabilities, and obligations as directly yours.

✅ Advantages

- Zero mandatory government registration fee

- No board meetings, no statutory audit

- Business losses offset personal income

- Complete operational freedom

- GST registration is sufficient to operate formally

⚠️ Limitations

- Unlimited personal liability — no legal separation

- Cannot raise equity investment

- Business ceases on owner’s death or incapacity

- Taxed at personal slab rates up to 30%

- Low credibility for B2B contracts and tenders

⚠️ Udyam / MSME Registration is optional, not mandatory. A sole proprietor can register under udyamregistration.gov.in to access MSME benefits — but this does not create a separate legal entity or limit liability.

2 What Is a Private Limited Company in India?

A private limited company is a separate legal entity incorporated under the Companies Act 2013. It has its own PAN, can own assets, enter contracts, and sue or be sued in its own name. Shareholders’ liability is limited to the amount unpaid on their shares — personal assets are protected.

3 Full Comparison Table: Sole Proprietorship vs Private Limited Company

This is the core of the sole proprietorship vs private limited company decision. Every key parameter — liability, tax, compliance, funding, and cost — compared side by side for business structure India 2026.

| Parameter | Sole Proprietorship | Private Limited Company |

|---|---|---|

| Legal Status | Not a separate legal entity | Separate legal entity under Companies Act 2013 |

| Registration Required | None mandatory GST / Udyam optional |

SPICe+ on MCA Portal Certificate of Incorporation issued |

| Liability | Unlimited Personal assets at risk |

Limited Up to shareholding value |

| Min. Owners | 1 (owner = business) | 2 directors + 2 shareholders |

| Tax Rate (2026) | Individual slab rates 5% → 30% depending on income |

22% + 10% surcharge + 4% cess Effective ~25.17% under Sec 115BAA |

| Dividend Tax | N/A (profits taxed directly) | Taxed in hands of shareholder at slab rate |

| Govt Setup Cost | ₹0 | ₹1,443+ (MCA fee) Varies with authorised capital |

| Annual Compliance | ITR-3/4, GST returns if applicable | MGT-7A, AOC-4, 4 board meetings, statutory audit |

| Statutory Audit | Not required (tax audit above ₹1 Cr threshold) | Mandatory every year |

| Equity Fundraising | Not possible | Fully supported |

| Bank Credit Ease | Based on personal credit | Company credit history, higher limits possible |

| Business Continuity | Dissolves on owner’s death | Perpetual succession |

| IPR / Trademark | Registered in owner’s personal name | Registered in company’s name |

| Foreign Investment (FDI) | Not permitted | Permitted under FEMA |

| Setup Timeline | 1–3 days (GST, bank account) | 5–7 working days (off-peak) |

Govt fee verified against mca.gov.in fee schedule. Tax rates as per Income Tax Act 1961 applicable for AY 2026-27. Always verify current rates at incometax.gov.in.

4 Tax Comparison 2026: Where the Real Difference Lies

Tax treatment is one of the most misunderstood aspects of the sole proprietorship vs private limited company debate. The choice is not simply about which structure pays less — it depends on your profit level, dividend strategy, and reinvestment plans.

Sole Proprietorship Taxation

A sole proprietor’s business income is treated as personal income and taxed at the applicable individual slab rate under the Income Tax Act 1961. Under the new tax regime for AY 2026-27, rates range from 5% on income above ₹3 lakh to 30% on income above ₹15 lakh. There is no separate corporate deduction — whatever the business earns, you pay tax on it at your personal rate.

Private Limited Company Taxation

A domestic private limited company opting under Section 115BAA pays a base corporate tax rate of 22%. Adding a 10% surcharge and 4% health and education cess, the effective rate comes to approximately 25.17%. New domestic manufacturing companies incorporated after 1 October 2019 and commencing production before 31 March 2024 were eligible for a 15% concessional rate under Section 115BAB — this window has now closed for new applicants.

📌 Key insight: Below ~₹20 lakh in net profit, a sole proprietor’s effective tax rate is often lower than the ~25.17% corporate rate. Above ₹20–25 lakh, a private limited company typically becomes tax-efficient — especially when profits are retained in the company rather than paid out as dividends.

Dividend distribution from a private limited company is taxable in the hands of shareholders at their applicable slab rate (post 2020 abolition of DDT). This creates potential double taxation — once at the corporate level and once when profits are distributed. However, founders who retain profits inside the company for reinvestment benefit from the lower corporate rate during the growth phase.

5 Liability Protection: The Decisive Factor for Most Founders

Unlimited liability is the single most compelling reason to incorporate a private limited company rather than operate as a sole proprietor. In a sole proprietorship, if the business incurs a debt, loses a lawsuit, or faces a regulatory penalty — your home, savings, and personal investments are all at risk.

🚨 Sole Proprietorship Risk Scenario

Your client sues for ₹50 lakh in damages over a contract dispute. As a sole proprietor, the court can attach your personal bank account, property, and assets to satisfy the claim. There is no legal firewall between you and the business.

🛡️ Private Limited Company Protection

The same ₹50 lakh claim is against the company’s assets only. As long as you haven’t personally guaranteed the debt or committed fraud, your personal assets are not reachable. This protection is established under Sections 34 and 36 of the Companies Act 2013.

⚠️ Personal guarantee exception: Banks and lenders frequently require director personal guarantees for loans to small private limited companies. In those cases, the director’s personal assets become exposed to the extent of the guarantee — so always negotiate guarantee terms carefully.

6 Annual Compliance: Cost and Effort Compared

Compliance cost is where the business structure India conversation gets practical. A private limited company carries a substantially higher compliance burden than a sole proprietorship — both in mandatory filings and in professional fees.

| Compliance Activity | Sole Proprietorship | Private Limited Company |

|---|---|---|

| Income Tax Return | ITR-3 or ITR-4 (annual) | ITR-6 (annual, company return) |

| Statutory Audit | Not required (optional tax audit above ₹1 Cr) | Mandatory every year |

| ROC Annual Return | Not applicable | MGT-7A — due within 60 days of AGM |

| Financial Statements Filing | Not required | AOC-4 — due within 30 days of AGM |

| Board Meetings | Not applicable | Minimum 4 per year (Section 173) |

| Director KYC | Not applicable | DIR-3 KYC annually (due 30 September) |

| GST Returns | As applicable (GSTR-1, GSTR-3B) | As applicable (same obligations) |

| Approx. Annual Professional Cost | ₹5,000–₹15,000 | ₹30,000–₹1,00,000+ |

7 Funding, Scalability & Business Continuity

If your business plan involves raising external capital — angel funding, venture capital, or even structured bank loans — a private limited company is the only viable business structure in India. Equity shares can be issued and transferred, which enables investment rounds, ESOPs, and strategic exits.

✅ DPIIT Startup Recognition: A private limited company (or LLP) can apply for DPIIT startup recognition on Startup India portal, unlocking tax exemptions under Section 80-IAC, self-certification for labour laws, and faster IPR processing. Sole proprietorships are not eligible for DPIIT recognition.

8 Decision Framework: Which Business Structure Should You Choose in 2026?

The right choice in the sole proprietorship vs private limited company debate depends on where you are in your business journey and what you’re building toward. Here is a structured decision framework for first-time founders.

🧭 Choose Sole Proprietorship If:

🚀 Choose Private Limited Company If:

Not Sure Which Structure Is Right for Your Business?

Our team analyses your business model, revenue projections, and tax position to recommend the correct structure — before you file a single form.

Get a Free Consultation → View Registration Services9 Conclusion: Sole Proprietorship vs Private Limited Company — Making the Right Call

The sole proprietorship vs private limited company decision is not a permanent one — you can always convert a proprietorship to a private limited company as your business grows. But making the wrong initial choice does create friction: missed tax optimization opportunities, lack of credibility in B2B deals, and exposure to personal liability that you could have avoided from day one.

For most first-time founders building a scalable product or service business in India in 2026, a private limited company is the structurally superior choice. It costs more to maintain, but it protects you, positions you for investment, and establishes the business as a credible, durable legal entity. The ₹1,443 minimum government fee and a week’s registration timeline are a small price for perpetual succession, limited liability, and the full optionality that a company structure provides.

If you are testing an idea with minimal capital, a sole proprietorship is a perfectly valid starting point — register for GST, build your revenue, and convert to a private limited company business structure in India once you have validated the market. What matters most is that you make the decision with accurate, current information — not assumptions built on outdated data or generic advice. Consult a qualified CA or company secretary before choosing your business structure for 2026.

10 FAQs — Sole Proprietorship vs Private Limited Company

Yes. Conversion is done by incorporating a new private limited company and transferring the business assets, contracts, and goodwill from the proprietorship to the new entity. There is no direct statutory conversion mechanism — it is a fresh incorporation followed by a business transfer agreement. GST and other registrations must be updated accordingly. Confirm the current SPICe+ process at mca.gov.in.

Yes. A sole proprietorship can register for GST under gst.gov.in using the proprietor’s PAN. The GST registration is issued in the business trade name but linked to the individual’s PAN. There is no requirement to incorporate a company before obtaining GST registration.

A domestic private limited company opting under Section 115BAA of the Income Tax Act pays 22% base corporate tax, plus a 10% surcharge and 4% health and education cess — giving an effective all-in rate of approximately 25.17%. Companies not opting for 115BAA pay the standard 30% base rate (plus surcharge and cess). Always verify current rates at incometax.gov.in before tax planning.

No. Foreign Direct Investment is not permitted in a sole proprietorship under FEMA regulations. Additionally, equity investment by Indian angel investors or venture capital funds requires an incorporated entity — a private limited company or LLP. A sole proprietorship can only accept debt, not equity capital.

A sole proprietorship has no legal existence separate from its owner. On the owner’s death, the business ceases to exist as a legal entity. Business assets pass to legal heirs through succession, but contracts, licences, and GST registrations cannot be transferred automatically. A private limited company, by contrast, has perpetual succession — it continues operating regardless of changes in ownership or the death of a director.

Late filing of MGT-7A (annual return) or AOC-4 (financial statements) attracts additional fees of ₹100 per day per form — there is no upper cap, making delays expensive quickly. Persistent non-compliance can lead to the company being struck off the register by the Registrar of Companies under Section 248 of the Companies Act 2013. Directors of struck-off companies face disqualification under Section 164(2). Verify current fee schedules at mca.gov.in.