GST Changes May 2026: All New Rules, Rates & Compliance Updates Every Business Must Act On

A complete, cross-verified guide to GST 2.0 reforms, Budget 2026 amendments, e-invoicing enforcement, ITC hard block, and what’s coming in the 57th GST Council Meeting

⚡ Key Takeaways — GST Changes May 2026

- GST 2.0: Four-slab structure (0%, 5%, 18%, 40%) is fully operational — the 12% slab is abolished.

- E-invoicing is now mandatory for all businesses with AATO above ₹5 crore (effective April 1, 2026).

- ITC Hard Block is live: mismatches between GSTR-2B and GSTR-3B will freeze your return filing.

- IMS (Invoice Management System): no action on an invoice is treated as deemed acceptance — unreviewed invoices auto-flow into GSTR-2B. Active weekly review of your IMS dashboard is mandatory.

- Budget 2026 amendments to Sections 13, 15, 34, and 54 of CGST/IGST Act are now in effect.

- The 57th GST Council Meeting is expected in late May or June 2026 — major compliance reforms anticipated.

If you are a business owner, accountant, or compliance professional in India, GST changes in May 2026 demand your immediate attention. The Indian GST regime has undergone its most sweeping transformation since the original rollout in 2017. Triggered by the 56th GST Council Meeting of September 2025, Budget 2026 amendments, and a series of CBIC notifications, GST new rules 2026 have fundamentally restructured how taxes are levied, how Input Tax Credit (ITC) is claimed, how invoices are managed, and how refunds are processed. This blog is a complete, fact-verified guide to every change that is currently in effect — and everything you need to do right now in May 2026 to stay compliant and avoid penalties.

1 GST 2.0: The New Rate Structure (Fully Effective)

The most consequential change in the GST changes May 2026 landscape is the complete restructuring of tax slabs. The 56th GST Council Meeting, held on September 3, 2025, approved the next-generation GST reform announced by Prime Minister Narendra Modi on Independence Day 2025. CBIC issued the formal notifications on September 17, 2025, and the new structure became effective from September 22, 2025. By May 2026, this structure is fully operational across all sectors.

| Old Slab | New Slab (GST 2.0) | Category | Key Examples |

|---|---|---|---|

| 0% | 0% (Nil) | Exempt / Essential | Unprocessed farm produce, public education, life & health insurance |

| 5% / 12% | 5% (Merit Rate) | Essential Goods & Services | Packaged grains, basic medicines, dairy products, 33 lifesaving drugs, healthcare services |

| 18% / 12% | 18% (Standard Rate) | Most Goods & Services | Electronics, construction materials (cement, steel), automobiles, most services, SaaS/digital services |

| 28% + Cess | 40% (Sin/Luxury) | Demerit / Luxury Goods | High-end automobiles, luxury vehicles (>1200cc/1500cc or >4000mm), luxury watches, aerated beverages, gambling. Cigarettes, pan masala, gutkha & chewing tobacco: 40% effective 1 Feb 2026 per Notification No. 19/2025-CTR (not Sep 22, 2025). |

| 28% | 18% | Bidis / Biris (Tobacco) | Bidis (biris) — moved from 28% to 18% effective 1 Feb 2026 per Notification No. 19/2025-CTR. This is separate from the 40% applicable to cigarettes and other tobacco products. |

| Special: 3% | 3% | Precious Metals | Gold jewellery, gold biscuits (HSN Chapter 71) — unchanged |

Businesses in affected sectors — particularly packaged food (5%), consumer electronics (18%), and construction materials (18%) — must review all product classification masters and update pricing contracts. Businesses dealing with goods that moved from 12% to 18% may need to renegotiate B2B contracts to account for the additional 6% cost impact.

2 E-Invoicing: Threshold Lowered to ₹5 Crore (Effective 1 April 2026)

One of the most operationally significant GST new rules 2026 is the expansion of mandatory e-invoicing. From April 1, 2026, e-invoicing is compulsory for any business with an Aggregate Annual Turnover (AATO) exceeding ₹5 crore in FY 2025-26.

₹5 Crore+ AATO

E-invoicing mandatory from 1 April 2026. All B2B invoices, credit notes, and debit notes must carry a valid IRN.

30-Day IRN Window

For businesses with AATO ≥ ₹10 crore: invoices must be reported to IRP within 30 days of invoice date. IRN generation is blocked beyond this window.

Case-Insensitive IRN

Invoice numbers are auto-converted to UPPER CASE before IRN generation. Systems with mixed-case invoice series must be standardised to avoid duplicate rejection errors.

Businesses that have never crossed ₹5 crore are not required to generate e-invoices — but must continue monitoring the threshold as it may be lowered further. All e-invoice-eligible businesses must generate IRN on the same day or next business day at the latest, to avoid breaching the 30-day window. Standardise invoice numbering governance across all ERPs, billing systems, and subsidiaries to prevent duplicate-invoice errors on the IRP portal.

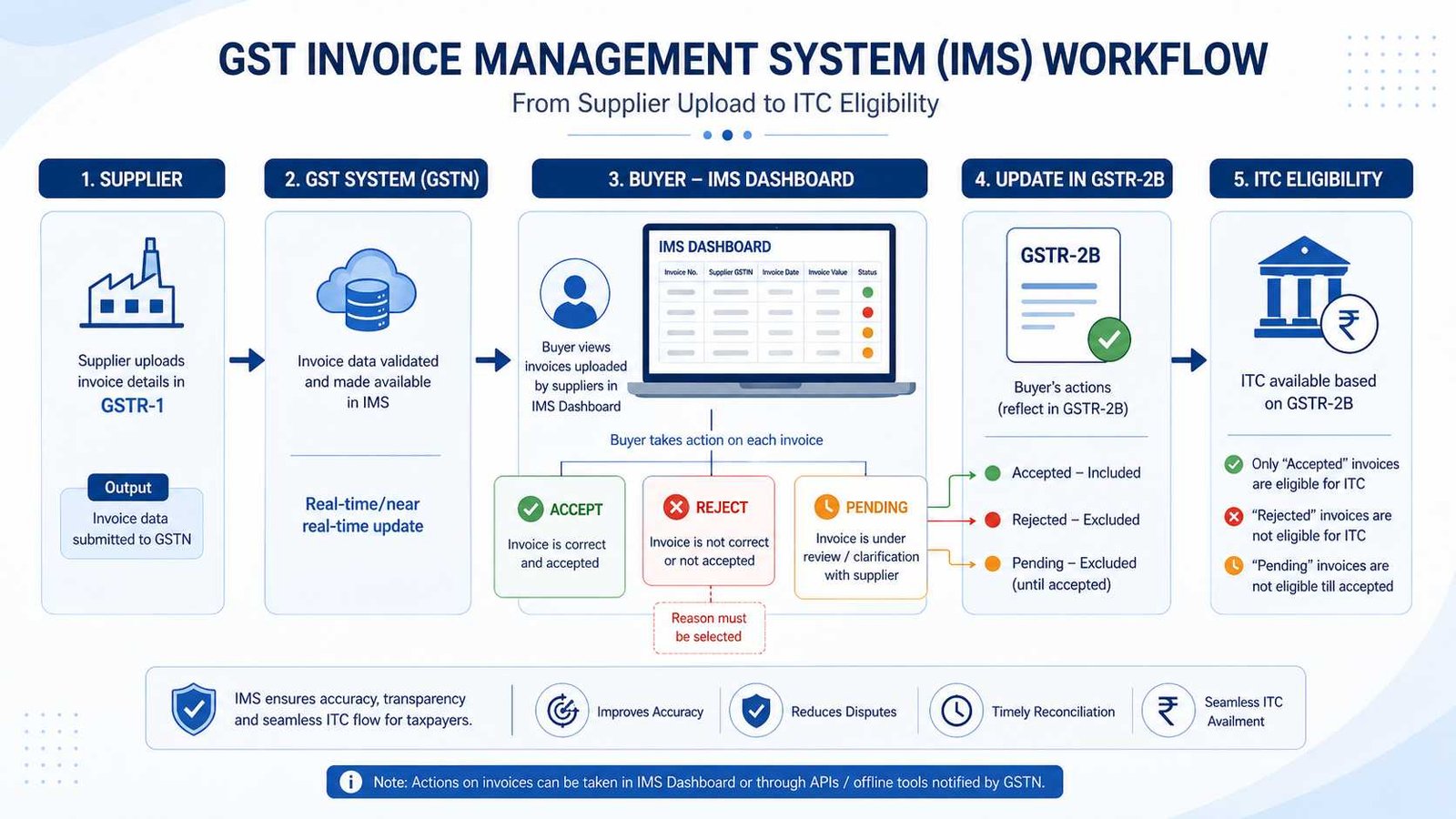

3 ITC Hard Block & Invoice Management System (IMS) — Zero Mismatch Policy

The GST changes in May 2026 that will have the sharpest cash-flow impact on businesses is the enforcement of the Zero Mismatch Policy and the full operationalisation of the Invoice Management System (IMS). These two changes together have ended the era of provisional ITC claims.

What Is the Zero Mismatch Policy?

From April 1, 2026, if there is any discrepancy between what your suppliers have reported in their GSTR-1 (reflected in your GSTR-2B) and what you have claimed in your GSTR-3B, the GST portal will hard-block your return filing until the error is corrected. There are no overrides, no grace periods, and no manual workarounds.

How IMS Works (Effective October 2024, Fully Enforced from April 2026)

The Invoice Management System sits between your supplier’s GSTR-1 filing and your GSTR-2B. Every invoice uploaded by a supplier appears in your IMS dashboard within 24 hours. You must take one of three actions on each invoice:

| IMS Action | Effect on Your GSTR-2B | Effect on ITC |

|---|---|---|

| Accept | Invoice flows into GSTR-2B | ITC eligible and claimable in GSTR-3B |

| Reject | Invoice removed from GSTR-2B | ITC not available; supplier notified |

| Keep Pending | Held out of GSTR-2B for current period | ITC deferred to next period |

| No Action (Inaction) | Treated as Deemed Accepted — invoice auto-flows into GSTR-2B | ITC populates automatically. Risk: incorrect/fraudulent invoices get accepted if not reviewed. Monitor IMS weekly. |

- Assign a dedicated team member to review IMS daily or at least weekly — monthly is no longer sufficient.

- GSTR-3B table values for outward supply liability are now auto-populated and hard-locked from GSTR-1 data. Manual overrides of Table 3 values are no longer possible (effective July 2025).

- Monitor supplier compliance weekly. If your supplier does not file GSTR-1 on time, you lose ITC for those invoices.

- Build a vendor compliance scorecard — onboard only GST-compliant vendors with a clean filing history.

4 Budget 2026 GST Amendments: Four Key Law Changes

The Finance Act 2026 enacted several CGST/IGST Act amendments that are now operational as of May 2026. These flow from the 56th GST Council Meeting’s recommendations and address long-standing disputes between taxpayers and tax authorities.

Post-Sale Discounts (Sec 15 & 34)

Businesses no longer need a pre-existing agreement to claim GST benefits on post-sale discounts. A credit note under Section 34 and ITC reversal by the recipient is sufficient to exclude the discount from taxable value.

Intermediary Services (Sec 13 IGST)

Place of supply is now the recipient’s location (not the supplier’s). Indian IT/ITES, marketing agencies, and back-office service providers working for foreign clients can now treat such services as zero-rated exports.

Inverted Duty Refunds (Sec 54)

Provisional refunds now cover inverted duty structure claims. Exporters receive 90% of eligible refund within 7 days (reduced from 14 days). The minimum ₹1,000 threshold for export refund processing has been removed.

Section 13 IGST Amendment — Major Relief for Indian Service Exporters

This is one of the most significant wins for India’s service export industry in the GST new rules 2026 package. Previously, intermediary services were taxed at 18% GST even when the client was overseas, because the place of supply was the supplier’s location (India). With the Budget 2026 amendment, the place of supply is now aligned with the recipient’s location. When the recipient is outside India, the supply qualifies as an export of service — zero-rated — and the business can claim ITC on all inputs used for providing such services. This directly benefits IT companies, consulting firms, digital marketing agencies, legal process outsourcing units, and any Indian entity acting as intermediary for an overseas client.

ISD (Input Service Distributor) Mandatory Registration

Corporate groups operating across multiple GSTINs must ensure that Input Service Distributors are separately registered and that ITC is distributed using the ISD mechanism. Failure to comply with ISD registration requirements results in ITC denial across group entities. This rule is actively enforced in FY 2026-27.

5 3-Year Return Filing Lock — What It Means in May 2026

One of the most underreported but high-risk GST changes May 2026 is the statutory 3-year return filing time-bar. This is now fully enforced at the portal level with no manual override possible.

The 3-year lock operates as follows across return types:

| Return Type | Lock Period | May 2026 Status |

|---|---|---|

| GSTR-1 (Monthly) | 3 years from month’s due date | March 2023 locked from April 11, 2026; April 2023 locks from May 11, 2026 |

| GSTR-3B (Monthly) | 3 years from month’s due date | March 2023 locked from April 20, 2026; April 2023 locks from May 20, 2026 |

| GSTR-9 (Annual) | 3 years from filing due date | FY 2020-21 locked from December 2025 |

| GSTR-9C (Reconciliation) | 3 years from filing due date | FY 2020-21 permanently locked |

Important for FY 2025-26 GSTR-9: The Annual Return and reconciliation statement (GSTR-9C) for FY 2025-26 must be filed by December 31, 2026. Mandatory CA certification for GSTR-9C has been reinstated from FY 2025-26 onwards for businesses with turnover above ₹5 crore. Businesses that relied on the waiver granted for FY 2022-23 and 2023-24 must now engage a Chartered Accountant for this filing.

6 GSTR-3B Auto-Population & ITC Reversal Statement Updates

Two portal-level changes that took effect from February 2026 onwards are now part of every monthly compliance cycle as of May 2026.

Auto-Population of Tax Liability Breakup in GSTR-3B

From the February 2026 tax period onwards, the GST portal auto-populates the “Tax Liability Breakup, As Applicable” section in GSTR-3B for any interest or tax liability belonging to a previous tax period being discharged in the current return. Taxpayers must open this tab on the payment page and click “SAVE” within the tab before filing. Skipping this step may result in a filing error or incorrect interest computation.

ECRS (Electronic Credit Reversal and Reclaimed Statement)

The ECRS tracks all ITC reversals made by a taxpayer and their subsequent reclaims. Currently, a negative closing balance in ECRS triggers a warning. The GSTN has signalled that this warning will shortly be upgraded to a hard filing block — similar to how the RCM ITC statement issue operates. Businesses must update the ECRS with accurate, document-level reversal data immediately and should not wait for a portal enforcement deadline to clean up this data.

• GSTR-1 for April 2026 → Due: 11 May 2026

• GSTR-3B for April 2026 → Due: 20 May 2026

• LUT for FY 2026-27 (if not already filed) → Overdue — File immediately

• IMS Review (all pending invoices) → Ongoing — Weekly obligation

7 57th GST Council Meeting: What to Expect (May–June 2026)

The 57th GST Council Meeting had not been held as of May 1, 2026. Sources cited by NDTV Profit indicate the meeting is likely to be convened in the last week of May or in June 2026, after the conclusion of state assembly elections in Tamil Nadu, Assam, Kerala, West Bengal, and Puducherry. Results are expected on May 4, 2026, and the Council requires the presence of at least 50% of its total members — with states holding two-thirds of the voting weight — making adequate state representation a scheduling prerequisite.

Senior government officials have confirmed that the rate rationalisation exercise is substantially complete following the 56th meeting. The 57th meeting is therefore expected to focus primarily on:

- Bringing electricity and natural gas within the GST ambit (currently excluded, causing ITC chain disruption for industries).

- Permitting refunds of accumulated ITC on input services — a long-standing working-capital blockage issue across industries.

- Streamlining registration, refund, and audit processes through rule and policy changes.

- Deciding the fate of the Compensation Cess, which expired on March 31, 2026. A Group of Ministers is exploring a replacement “health and clean energy” cess — any such replacement would require a constitutional amendment.

- Potential GST Amnesty Scheme for procedural and technical non-compliances from the first 2-3 years of GST (FY 2017-18 to FY 2019-20).

- Clarification on valuation mechanism for renewable energy devices.

8 Other Notable GST Changes Active in May 2026

GTA Forward Charge Option (FY 2026-27)

Goods Transport Agencies can opt to pay GST under the forward charge mechanism for FY 2026-27. If your GTA has exercised this option, you must obtain a written declaration from them. Without this declaration, the reverse charge liability shifts to you as the recipient, and failure to self-invoice and pay GST under reverse charge triggers demand, interest, and penalty.

Fresh Invoice Document Series from 1 April 2026

All businesses must start a new document series from April 1, 2026, for invoices, debit notes, and credit notes. Continuing the FY 2025-26 series into FY 2026-27 creates reconciliation errors in GSTR-1 and can attract departmental scrutiny. This is one of the most commonly overlooked compliance requirements at the start of a new financial year.

Digital Services (OIDAR) Clarity

Online Information and Database Access or Retrieval (OIDAR) services provided by foreign companies to Indian consumers continue at 18%. The 2026 rules provide clearer guidance on what constitutes an OIDAR service and the obligations of e-commerce operators acting as intermediaries. For Indian SaaS companies, cloud computing providers, and AI-powered tool providers, the place of supply for B2B digital services follows the recipient’s location, while B2C digital services are taxed at the consumer’s location.

Cryptocurrency and Exchange Transactions

As confirmed by available GST guidance, exchange commissions and service charges on cryptocurrency transactions attract 18% GST. The underlying crypto asset transfer is treated as a supply of goods for GST purposes when traded on Indian exchanges. Cryptocurrency trading platforms are within the scope of GST compliance, including registration, return filing, and e-invoicing requirements where applicable.

Rule 14A Exit Simplified

Taxpayers registered under the simplified CGST Rule 14A route (3-working-day registration for small suppliers with output tax liability below ₹2.5 lakh per month) can now exit the scheme after filing returns for just one complete tax period, reduced from the earlier requirement of three months. The withdrawal takes effect from the first day of the month following approval.

9 GST Compliance Timeline — May to December 2026

-

11 May 2026

GSTR-1 filing deadline for April 2026 (monthly filers). Ensure all B2B invoices with IRNs are uploaded. IMS reconciliation must be complete before this date.

-

20 May 2026

GSTR-3B filing deadline for April 2026. ITC claimed must match GSTR-2B exactly. Hard block will prevent filing if there is a mismatch.

-

Late May / June 2026

Expected 57th GST Council Meeting. Likely agenda: electricity/gas under GST, compensation cess replacement, compliance simplification, and possible amnesty scheme.

-

Monthly (11th & 20th)

Ongoing: GSTR-1 by 11th; GSTR-3B by 20th; weekly IMS review; 30-day IRN window monitoring for ₹10 crore+ businesses.

-

31 December 2026

GSTR-9 Annual Return and GSTR-9C (with mandatory CA certification for >₹5 crore turnover) for FY 2025-26 due.

Need Help Navigating GST Changes in May 2026?

Our GST compliance experts at Validraft can audit your current setup, correct rate classifications, ensure e-invoice compliance, and keep your ITC clean. Get a free compliance review today.

Book a Free GST Compliance Review →Conclusion

The GST changes May 2026 represent a fundamental shift from a returns-based system to a technology-driven, real-time compliance architecture. The four-slab GST 2.0 structure, mandatory e-invoicing for ₹5 crore+ businesses, IMS-enforced ITC validation, and the automated Zero Mismatch Policy collectively mean that errors, mismatches, and delays have immediate financial consequences — blocked returns, frozen working capital, denied ITC, and automated penalties.

Budget 2026 amendments have also brought significant relief: service exporters benefit from the intermediary services place-of-supply correction, businesses with inverted duty structures get faster provisional refunds, and post-sale discount treatment is now simpler. The anticipated 57th GST Council Meeting in late May or June 2026 could bring additional reforms on compliance simplification, energy inclusion under GST, and an amnesty scheme for older technical defaults.

For every business — from MSMEs to large corporates — the only safe approach to GST new rules 2026 is proactive action: update your ERP and invoicing systems, train your accounts team on IMS workflows, build vendor compliance monitoring, clear all pending older-period returns before the 3-year lock closes them, and engage qualified GST professionals for your annual filings. Businesses that invest in compliance now will avoid penalties, maintain uninterrupted ITC cash flows, and be well-positioned for any further reforms that the 57th GST Council Meeting introduces.

Frequently Asked Questions

Government & Authoritative Sources

- GST Council — Official Meeting Records & Recommendations (gstcouncil.gov.in)

- CBIC — Central GST Notifications including No. 19/2025-CTR (Tobacco, effective 1 Feb 2026) (cbic-gst.gov.in)

- GSTN — GST Portal, IMS Advisory (Official: No Action = Deemed Acceptance), e-Invoice Advisory (gst.gov.in)

- GSTN — Revised Official IMS Advisory PDF (tutorial.gst.gov.in)

- Invoice Registration Portal — IRP for e-Invoice Generation (einvoice.gst.gov.in)

- E-Way Bill System — GSTN (ewaybill.gst.gov.in)

- PIB — 56th GST Council Meeting Press Release (pib.gov.in)

Disclaimer: This blog is for informational purposes only and does not constitute legal or tax advice. GST law is subject to frequent change. Always verify the latest CBIC notifications before making compliance decisions. Consult a qualified GST practitioner for specific guidance.