GST Changes April 2026: e-Invoicing, LUT Filing & Invoice Reset — Complete Guide

GST Changes from April 2026:

e-Invoicing, LUT Filing, Invoice Reset — Complete Guide

Every GST-registered business in India must act on four critical year-start obligations from April 1, 2026. Miss any one and face invalid invoices, blocked ITC, or export disruptions — all avoidable with a 15-minute compliance check.

e-Invoicing

Mandatory Threshold

LUT Grace Period

(Must File Before Export)

IRP Upload Window

for ₹10Cr+ Businesses

Refund Minimum

Removed (All Claims Valid)

- LUT for FY 2026-27 must be filed before generating any export invoice from April 1. The FY 2025-26 LUT expired on March 31, 2026 and carries no carryover validity. File free at gst.gov.in → Services → User Services → Furnish Letter of Undertaking.

- All invoice, debit note, and credit note series must be reset to a fresh sequence from April 1. Continuing the March 2026 series into April creates reconciliation errors in GSTR-1 and flags audit risk.

- e-Invoicing is mandatory for all businesses whose aggregate annual turnover (AATO) exceeded ₹5 crore in any financial year from FY 2017-18 onwards. This is not new for most — but businesses crossing the threshold for the first time in FY 2025-26 must register on the IRP before issuing any invoice from April 1.

- Businesses with AATO above ₹10 crore must upload invoices to the IRP within 30 days of the invoice date. Invoices uploaded after this window are rejected by the IRP and treated as invalid — buyers lose ITC on them.

- The ₹1,000 minimum threshold for export refunds has been removed. All valid refund claims — regardless of amount — must now be processed from April 1, 2026.

- ECRS negative balance warnings may soon block GSTR-3B filing. The GST portal has signalled hard validation in place of warnings for ECRS and RCM liability mismatches. Update your ECRS now.

The GST changes from April 2026 are not a single notification — they are a set of year-start obligations, threshold triggers, and portal enforcement upgrades that collectively affect every GST-registered business in India. Four are immediately actionable: LUT filing, invoice series reset, e-invoicing 5 crore compliance, and IMS obligations. Two more — ECRS hard validations and export refund rule changes — require internal system checks. None of these are optional, and several carry immediate financial consequences for non-compliance.

This guide covers every GST change effective April 1, 2026 in the order of operational urgency — starting with what must have been done on day one, through to the GSTR-1 and portal changes that affect monthly return filers throughout FY 2026-27.

1 LUT Filing for FY 2026-27 — Zero Grace Period Urgent

A Letter of Undertaking (LUT) allows exporters and businesses supplying to SEZ units to make zero-rated supplies without paying IGST upfront. Without a valid LUT, every such supply is treated as a taxable supply — meaning IGST must be paid first and a refund claimed later, blocking working capital for weeks or months.

The LUT filed for FY 2025-26 expired on March 31, 2026. It does not automatically roll over to the new financial year. Any business that made zero-rated supplies without a valid FY 2026-27 LUT from April 1 has already created a compliance gap. Filing one now before the next export invoice is the immediate fix.

| Step | Action | Where |

|---|---|---|

| 1 | Log in to the GST portal | gst.gov.in |

| 2 | Navigate to Services → User Services | GST Portal Dashboard |

| 3 | Select “Furnish Letter of Undertaking (LUT)” | User Services dropdown |

| 4 | Select FY 2026-27, fill the form, submit with DSC or EVC | GST Portal Form |

| 5 | Download and save the LUT reference number as proof | GST Portal Downloads |

✅ Cost: LUT filing is completely free. It takes under 10 minutes on the GST portal. There is no fee, no professional certification required, and no document upload — just the GSTIN, declaration, and digital signature.

🚨 If you exported without a valid LUT from April 1: Those supplies are treated as taxable. IGST liability attaches retrospectively. File the LUT immediately, then assess whether a refund claim or amendment is needed for any invoices already raised without it.

2 Invoice Numbering Reset — Mandatory from April 1, 2026

GST compliance norms require every registered taxpayer to begin a fresh document series for invoices, debit notes, and credit notes from the start of each financial year. This is not a new rule — but it is routinely violated by businesses that continue the previous year’s number sequence out of habit or because their billing software defaults to the existing series.

Using March 2026’s invoice series in April 2026 creates direct problems: reconciliation mismatches in GSTR-1 between the invoice number on file and the reported series, potential IRP rejection for e-invoice filers whose systems detect a non-reset sequence, and audit flags during departmental scrutiny of outward supply records.

📌 Multi-GSTIN businesses: Each GSTIN operates an independent document series. If your business has multiple registrations — manufacturing units in different states, for instance — verify that the series reset has been applied to every GSTIN separately.

3 e-Invoicing 5 Crore Threshold — Who Must Comply from April 1

e-Invoicing under GST has expanded in phases since 2020. The current mandatory threshold stands at ₹5 crore of aggregate annual turnover (AATO) — calculated across all GSTINs under the same PAN. This is not a new threshold as of April 2026, but it becomes newly applicable to every business whose AATO first crossed ₹5 crore in FY 2025-26. Those businesses were not covered in FY 2025-26 but must generate e-invoices for every B2B, export, and SEZ supply from April 1, 2026.

| AATO Threshold | e-Invoicing Obligation | 30-Day IRP Upload Rule |

|---|---|---|

| Below ₹5 crore | Not mandatory (voluntary possible) | Not applicable |

| ₹5 crore to ₹10 crore | Mandatory — B2B, exports, SEZ supplies | No specific 30-day rule |

| Above ₹10 crore | Mandatory — B2B, exports, SEZ supplies | Yes — upload within 30 days of invoice date or IRP rejects |

The e-invoicing 5 crore rule applies even if current-year turnover drops below the threshold. Once a business has crossed ₹5 crore in any financial year since FY 2017-18, it remains within the e-invoicing framework. There is no exit mechanism once covered.

⚠️ Non-compliance penalty: Failure to generate a valid e-invoice where mandatory renders the invoice invalid for GST purposes. The buyer cannot claim ITC on it. A penalty of ₹10,000 per instance can apply under Section 122 of the CGST Act for incorrect or missing e-invoices.

4 30-Day IRP Upload Rule — Critical for ₹10 Crore+ Businesses

For businesses with AATO above ₹10 crore, the 30-day rule for uploading invoices to the Invoice Registration Portal has been in force since April 1, 2025 and continues unchanged in FY 2026-27. An invoice not uploaded to the IRP within 30 days of its date will be rejected by the portal — no IRN is generated, the invoice carries no QR code, and it cannot be used to support an ITC claim by the buyer.

The practical implication for ₹10 crore+ businesses is that invoice generation and IRP upload must be integrated as a single workflow — not a periodic batching exercise. Businesses that upload invoices in bulk at the end of the month risk missing the 30-day window for invoices raised early in the previous month.

Need a GST Compliance Check for April 2026?

Validraft’s GST team reviews your LUT status, invoice series, e-invoicing setup, and IMS obligations — then clears every gap before your next GSTR-1 filing cycle.

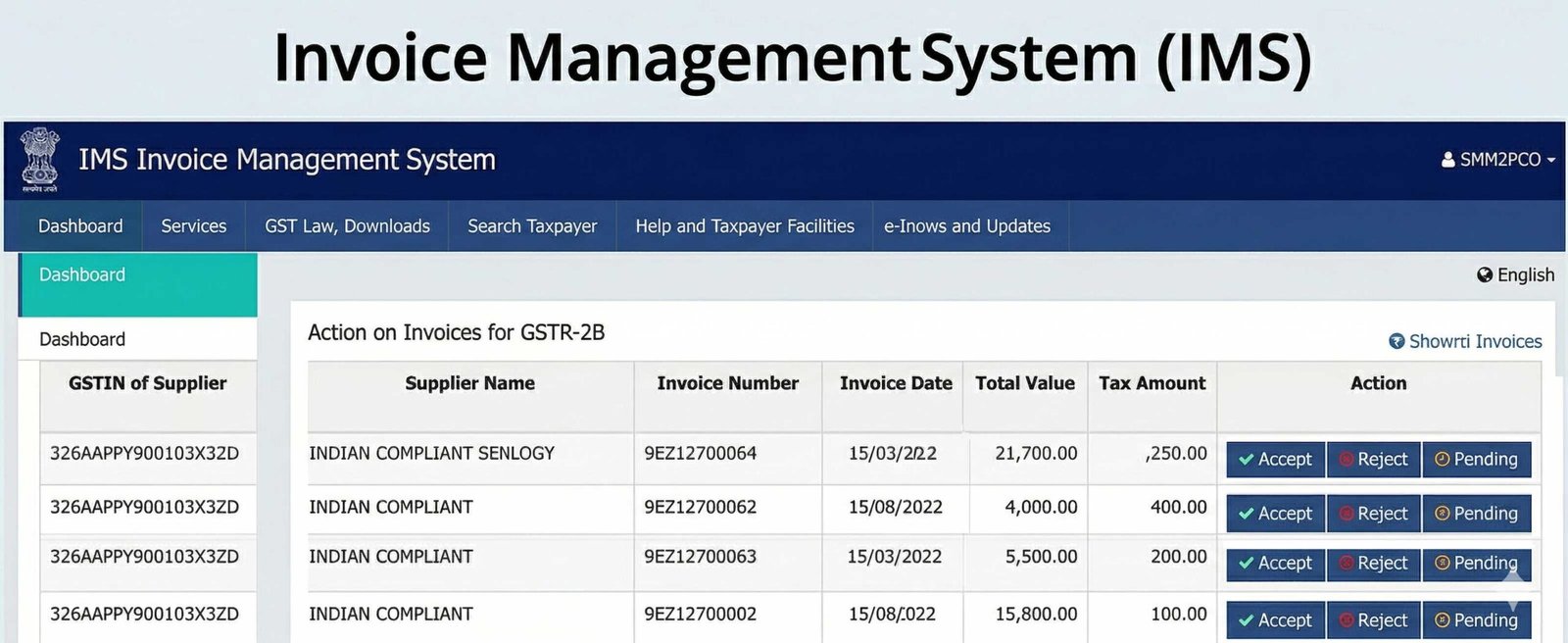

Book a GST Review → View GST Services5 IMS Obligations — Invoice Management System in FY 2026-27

The Invoice Management System (IMS) on the GST portal became operational in October 2024 and is now a live, active component of monthly GSTR-2B generation and ITC claiming. Understanding how IMS works is not optional for any business filing monthly returns — inaction on IMS has direct consequences for GSTR-3B liability and ITC availability.

The ECRS (Electronic Credit Reversal and Reclaimed Statement) is also live and tracking ITC reversals. The GST portal has issued an advisory that negative closing balances in the ECRS — which currently produce warnings — may soon trigger a hard block on GSTR-3B filing. Review and update ECRS with accurate document-level data throughout FY 2026-27 to avoid a filing block mid-year.

6 Export Refund Rule Change — ₹1,000 Minimum Removed

A long-standing restriction under GST law prevented the processing of export refund claims below ₹1,000. This affected small exporters, freelancers exporting services, and startups whose individual transaction refund amounts fell below the threshold — resulting in small but legitimate tax amounts being permanently forfeited.

From April 1, 2026, this ₹1,000 minimum threshold has been removed from the law. Every valid export refund claim — regardless of amount — must now be processed. For small service exporters and businesses with multiple lower-value export invoices per month, this is a meaningful recovery opportunity. All prior unprocessed claims below ₹1,000 should be reviewed to assess whether resubmission is applicable.

✅ Action item: Review all previously unfiled or rejected export refund claims below ₹1,000 for periods where the limitation was in effect. Consult with a GST professional to assess whether retrospective resubmission is possible for eligible claims. File new refund applications at gst.gov.in → Services → Refunds.

7 HSN Code Reporting in GSTR-1 — What’s Required in FY 2026-27

Mandatory HSN code reporting in Table 12 of GSTR-1 has been implemented in phases since 2022. Phase 3, effective from the May 2025 return period, made HSN code selection from a dropdown mandatory — manual entry of HSN codes is no longer permitted in GSTR-1 Table 12. The turnover-based digit requirement continues unchanged for FY 2026-27:

Table 12 in GSTR-1 is now split into “B2B Supplies” and “B2C Supplies” tabs — HSN summaries must be reported separately for each category. Table 13 (list of documents issued) is also mandatory from the May 2025 return period for all filers. Verify that your GSTR-1 filing software correctly handles the split Table 12 and populates Table 13.

8 GST Changes April 2026 — Full Action Checklist for Business Owners

GST Changes April 2026 — Let Validraft Handle Your Compliance

LUT filing, e-invoicing registration, GSTR-1 review, and IMS setup — Validraft covers all GST year-start obligations for FY 2026-27 in one engagement.

Start My GST Compliance → GST Filing Services9 Frequently Asked Questions — GST Changes April 2026

10 Conclusion: Every GST Change April 2026 Requires Action — Not Monitoring

The GST changes from April 2026 are not regulatory updates to read and file away — each one has an immediate operational trigger. LUT filing must precede the first export invoice. The invoice series reset must be configured before the first invoice of April. The e-invoicing 5 crore threshold must be checked against FY 2025-26 AATO, and any business newly covered must be IRP-registered and integrated before issuing supplies. For ₹10 crore+ businesses, the 30-day IRP upload rule requires a workflow change, not a reminder.

The IMS is now an active compliance layer that sits between supplier GSTR-1 uploads and your GSTR-2B ITC. A business that ignores the IMS dashboard through Q1 FY 2026-27 risks either claiming incorrect ITC or missing legitimate credit that was pending and eventually lapsed. The ECRS negative balance risk adds another monitoring obligation — one the GSTN has signalled may become a hard filing block.

Validraft handles GST year-start compliance for businesses across India — LUT filing, e-invoicing registration, IMS setup, GSTR-1 review, and ongoing monthly return support. If your business needs a structured GST compliance engagement for FY 2026-27, or if any of the GST changes April 2026 have created an unresolved gap, reach out before it appears in a department notice.